At some point, many people find themselves looking at their 401(k) and wondering: Could I just use that?

Maybe it’s an unexpected expense. Maybe it’s a transition period. Or maybe it’s an old account from a previous employer that feels disconnected from your day-to-day financial life.

And that’s often the moment when a decision is made and the 401(k) is no longer viewed as future income, but as available cash.

Before you tap your 401(k) account, it’s worth taking a closer look at what that money really represents.

Key Takeaways

- Your 401(k) is future income, not a reserve for short-term cash

- The true cost of withdrawing early is often what that money could have become

- Even ‘forgotten’ accounts can meaningfully support you later

- More flexibility doesn’t always lead to better decisions

- Thoughtful planning helps you solve for today without compromising tomorrow

A Different Way to Think About Your 401(k)

A 401(k) isn’t just another account. It’s one of the few places in your financial life specifically designed to support you later when your income from work slows or stops.

It works quietly in the background, benefiting from tax advantages and time. And time, more than anything, is what makes it powerful.

When you withdraw early, you’re not just accessing money. You’re curtailing the time those funds can grow.

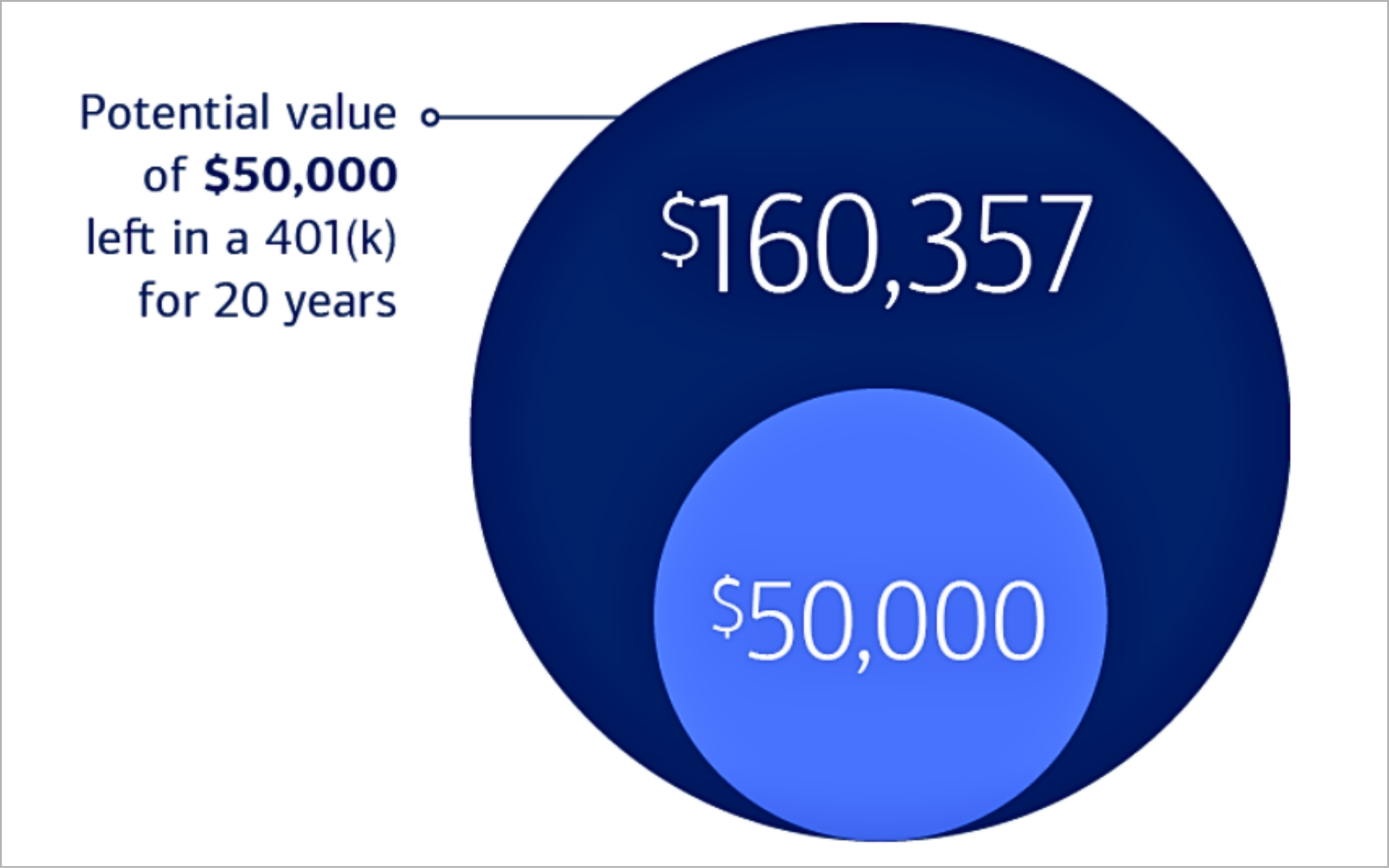

What It Can Cost You Later

Early withdrawals tend to come with visible costs—income taxes, and in many cases, a penalty if you’re under age 59½.

Though, the less visible cost is often more significant.

Money that stays invested has the potential to grow, and that growth compounds over time. When funds are pulled out early, you’re losing an opportunity to potentially grow your savings and investments.

Source: Merrill Lynch, 2026.

Notes: Assumes 6% annual investment returns. This example is hypothetical and for illustrative purposes only. It does not represent the performance of a particular investment. Actual investing includes fees and other expenses that may result in lower returns.

Access Has Expanded and So Has Temptation

In recent years, it’s become easier to access retirement funds. Plan features often allow for online withdrawals for hardship withdrawals, loans, and other emergency provisions.

These options can be helpful in true need.

But they also make it easier to solve short-term problems with long-term resources.

Just because something is accessible doesn’t mean it’s aligned with your goals.

Consider the Alternatives First

Before tapping your 401(k), it’s worth exploring other options that may preserve your long-term savings, such as:

- Adjusting current cash flow or spending

- Building or using an emergency fund

- Exploring short-term financing options

- Evaluating insurance or other available resources

Each option has trade-offs, but keeping your retirement savings intact whenever possible can make a meaningful difference down the road.

When a Withdrawal May Be Necessary

There are situations where using 401(k) funds is part of the conversation, particularly in cases of significant financial hardship.

If that’s the case, it’s important to clearly understand the trade-offs. Withdrawals are typically subject to income tax, and depending on your age and circumstances, may include additional penalties. Unlike a loan, the money generally can’t be put back once it’s taken out.

That doesn’t make it the wrong decision, but it does make it one worth approaching thoughtfully.

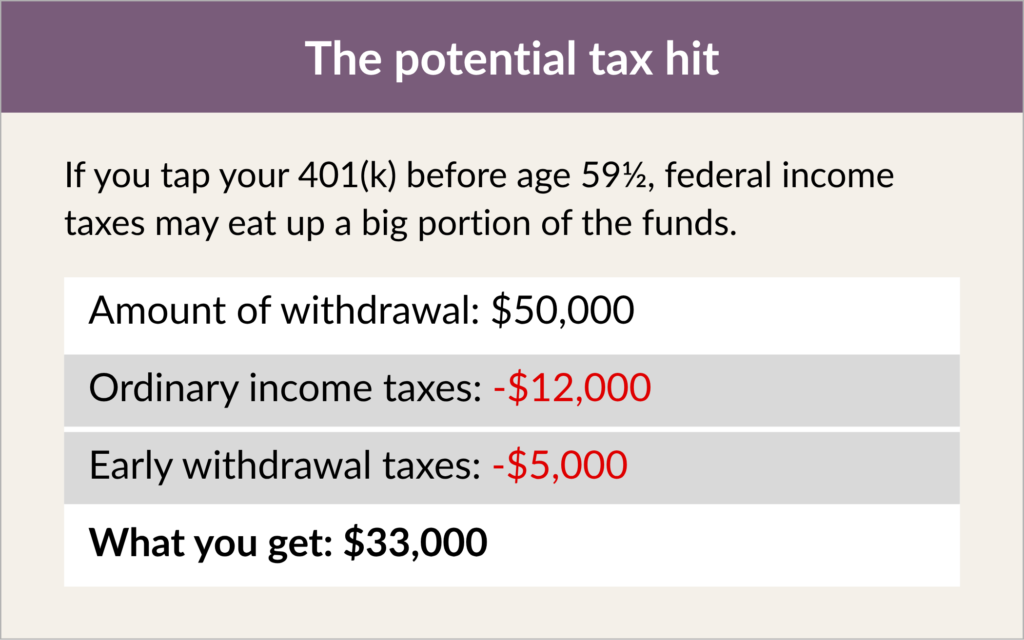

Your Potential Tax Hit

Consider the trade-off in the following example showing an early withdrawal (before age 59½) of $50,000 from a 401k:

Notes: Assumes a distribution of pre-tax funds, the account holder is under age 59½ (and no exception to the 10% additional tax applies) and has a 24% effective federal income tax rate; all tax calculations are estimates and should not be relied upon for detailed tax planning purposes.

Unfortunately, an early withdrawal nets you only a fraction of the spending power of the money you’re taking from your retirement savings.

Looking at the Full Picture

Before deciding, it can help to zoom out.

Are there other ways to meet the need that don’t disrupt long-term savings? Is this a one-time situation, or part of a larger cash flow challenge? How does this decision affect the next five, ten, or twenty years?

Those are the kinds of questions that shift this from a quick fix to a more intentional choice.

The Bottom Line

Your financial life will change over time. Needs will come up. Priorities will shift.

The goal isn’t to avoid every difficult trade-off. It’s to make decisions with a clear understanding of what you’re gaining, and what you may be giving up.

A financial planner can help you evaluate the trade-offs and how they may affect your long-term financial goals.

Frequently Asked Questions

Can I withdraw money from my 401(k) before retirement?

Yes, but withdrawals are typically subject to income tax and, if you’re under age 59½, may include a 10% penalty unless an exception applies.

Is it a good idea to cash out a 401(k) early?

In most cases, it can set back long-term retirement savings due to lost growth and tax consequences.

What happens if I take money out of my 401(k) early?

You may owe taxes, incur penalties, and reduce the amount available for future retirement income.

Is a 401(k) loan better than a withdrawal?

Loans can be repaid, which may reduce long-term impact, but they still carry risk, especially if employment changes before repayment.

What should I do with an old 401(k)?

Common options include rolling it into a current employer plan or an IRA, or leaving it in place, depending on your broader financial strategy.

0 Comments