In this review, we look back at the drivers of first quarter performance and discuss how recent developments may shape the outlook for the remainder of 2026.

Key Takeaways

- The first quarter was defined by sharp market volatility driven by renewed U.S. trade policy shocks and a major geopolitical escalation in the Middle East that disrupted global oil supplies.

- A quarter focused on waves from the AI boom and expected interest rate cuts changed to one driven by the Iran conflict and the oil price shock.

- Looking ahead, Q1 earning announcements begin the week of April 13. Elevated oil prices may prompt more conservative guidance amid uncertainty, while weakening macro conditions with slowing growth, resurfacing inflation, and higher rates create a more constrained policy environment for the Fed.

The first quarter of 2026 began with strong momentum across global equity markets, particularly outside the United States. Developed international and emerging market equities rose more than 15% and 12%, respectively, early in the year.

This strength was supported by a weakening U.S. dollar, attractive relative valuations, and improving economic conditions abroad. Expectations for policy easing in the U.S. provided an additional tailwind for global markets and certain segments of the U.S. market. However, this positive backdrop shifted as geopolitical tensions escalated with the onset of conflict in the Middle East. This introduced a new layer of uncertainty for investors.

Policy Uncertainty and Energy Shock Drive Volatility

Investors experienced increased volatility during the first quarter as markets navigated shifting trade policy and a significant geopolitical shock.

Trade tensions resurfaced following a February U.S. Supreme Court ruling that the International Emergency Economic Powers Act (IEEPA) does not authorize presidential tariffs. In response, the administration implemented a flat 10% tariff on most imports using alternative authority, adding another layer of policy uncertainty for markets.

The most significant development, however, was the escalation of conflict in the Middle East. Damage to key energy infrastructure and the effective closure of the Strait of Hormuz—a critical passage for global oil shipments—led to a meaningful supply disruption. Brent crude oil prices rose sharply during the quarter, increasing approximately 60% in March alone. This surge helped drive the Bloomberg Commodity Index higher by roughly 24% for the quarter, making commodities one of the strongest performing asset classes. Grain prices also rose, reflecting the Strait’s importance in transporting agricultural inputs.

Rising commodity prices have driven strong returns in this segment of the market. However, they are also contributing to a more fragile global backdrop. Disruptions to energy flows and supply chains are extending far beyond financial markets, and the broader consequences of the conflict, including the human impact, remain significant and cannot be overlooked.

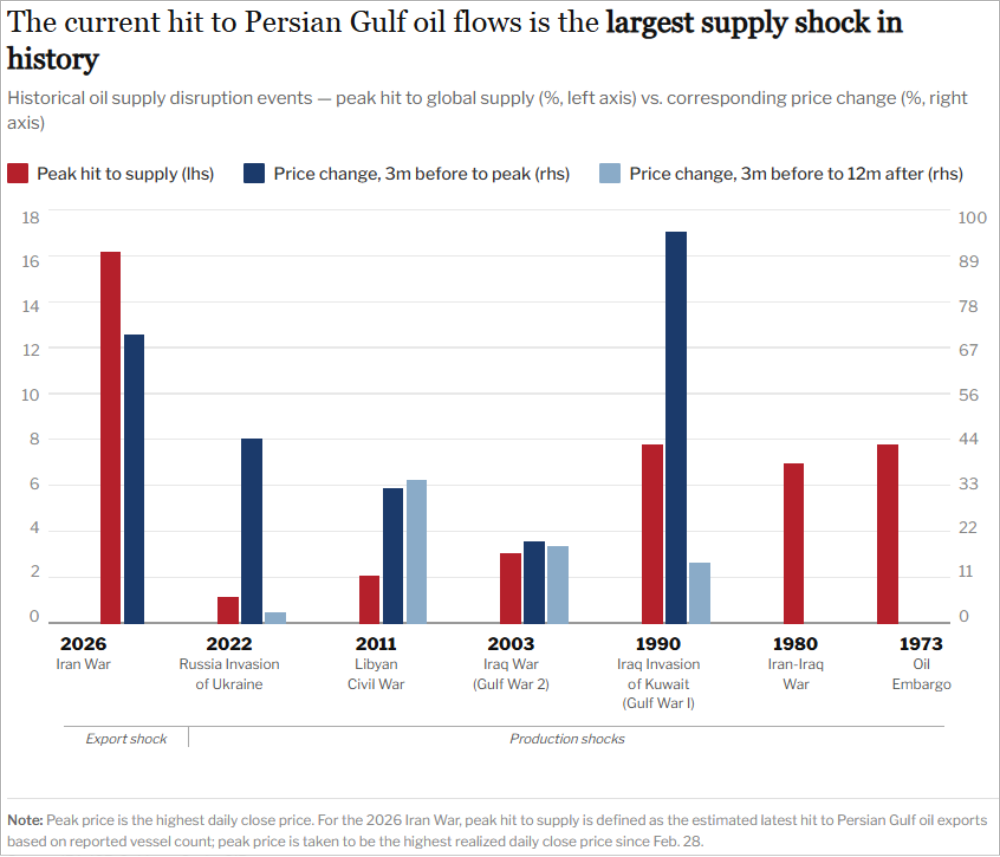

Middle East Conflict Disrupts Global Energy Supply

The geopolitical backdrop shifted meaningfully at the end of February when the U.S. and Israel launched attacks on Iran. Since then, market attention has focused on the Strait of Hormuz, a critical passage through which roughly 20% of global oil and a significant portion of liquefied natural gas shipments move each day.

Initially, investors expected the conflict to be short-lived, with energy flows resuming relatively quickly. More than a month later, the situation remains unresolved. The Strait has remained largely closed, and the extent of infrastructure damage appears greater than initially anticipated.

Higher energy prices have begun to work through the global economy. Consumers are seeing higher fuel costs, while businesses are facing increased transportation and input expenses. These pressures may also extend to food prices over time as agricultural input costs rise. The magnitude of the current disruption is notable in a historical context. As shown in the chart below, the estimated impact to global oil supply appears to exceed prior geopolitical events. While the price response has been significant, it has not yet reached the levels seen in some past shocks, suggesting markets may still be adjusting to the full impact of the disruption or are expecting tensions to ease over the near term.

Source: IEA, ICE, Goldman Sachs GIR.

Equity and Fixed Income Performance

Markets started the year on solid footing but became more volatile as the quarter progressed. Early optimism around global growth and easing policy expectations shifted toward concerns about rising energy prices and the potential for renewed inflation pressures.

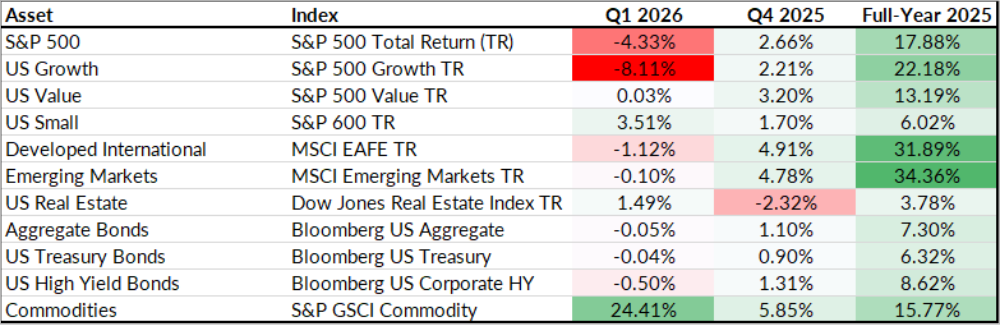

International equities were a good example of this shift. Developed and emerging market stocks posted strong gains in January and February but gave back much of those gains in March as geopolitical tensions escalated. For the quarter, developed markets declined -1.12% and emerging markets were down -0.10%, holding up better than U.S. stocks overall.

In the U.S., the S&P 500 declined -4.33%, driven largely by weakness in growth stocks, which fell -8.11%. Value stocks were relatively stable, finishing the quarter near flat, while small-cap stocks were a bright spot, gaining 3.51%.

Fixed income markets also experienced increased volatility. The Bloomberg U.S. Aggregate Bond Index was essentially flat for the quarter, down -0.05%, as rising short-term interest rates offset the benefit of higher starting yields.

Commodities were the clear standout, rising 24.41% during the quarter, driven primarily by the sharp increase in energy prices.

Quarterly Market Performance

Source: YCharts. Data as of 03/31/2026.

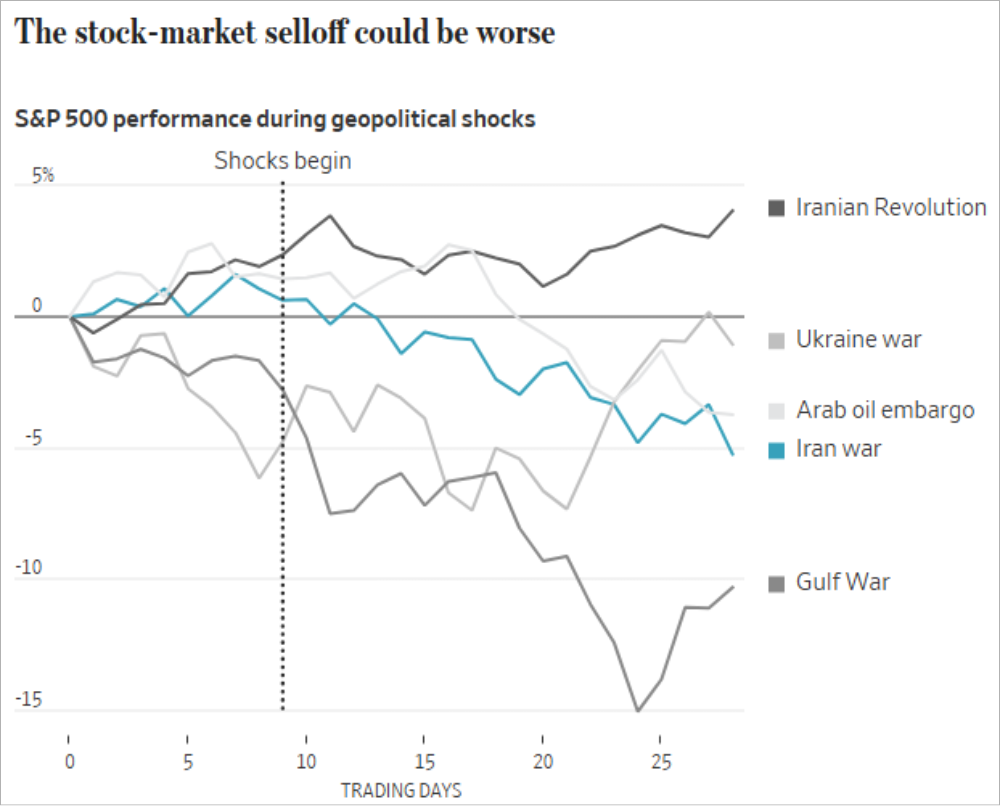

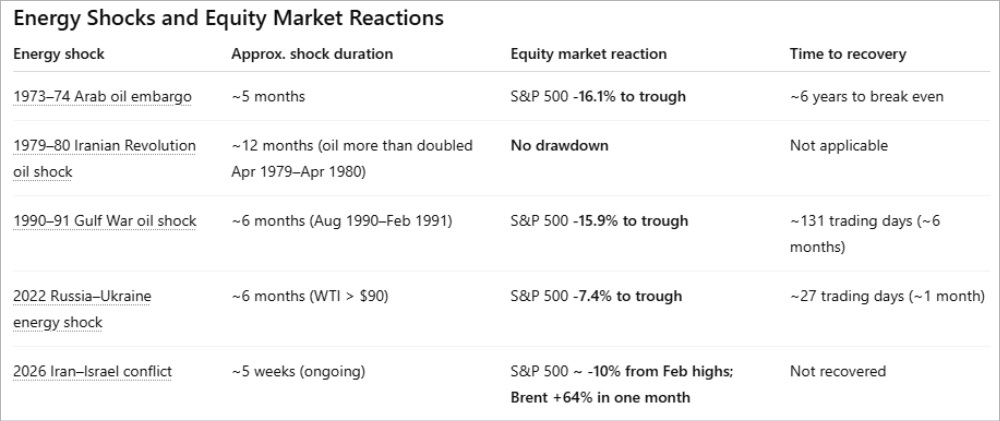

What History Suggests About Market Reactions

While the market pullback in March felt sharp, the pattern is not unusual when viewed in the context of past geopolitical events. Historically, and unsurprisingly, equity markets tend to weaken into these events and often see additional pressure in the days immediately following.

Source: “How Iran Compares With Past Market Shocks, in Charts,” WSJ.com, March 26, 2026.

The chart above illustrates this clearly across a range of shocks. From the Arab oil embargo to the current Iran conflict, the initial reaction is typically a drawdown in the mid-single digits within the first month of rising energy prices.

What matters more than the initial drawdown is how long the shock lasts. As the below chart shows, shorter disruptions, like the Gulf War or the Russia–Ukraine spike, saw markets recover in a matter of weeks to months, while more prolonged shocks led to deeper and longer market selloffs. With a two-week ceasefire recently announced, markets appear to be pricing this closer to a contained, shorter-duration shock rather than the start of a prolonged disruption. That said, conditions in the Middle East and market reactions can change quickly.

Source: Bloomberg, JPMorgan Asset Management, Barclays Private Bank, Federal Reserve, Reuters, 2026.

Looking Ahead: What Has Changed and What Comes Next

Coming into 2026, we expected a continuation of the current expansion, even after three consecutive years of strong equity returns and higher equity valuations. The view was supported by the expectation of continued strong corporate earnings both in the U.S. and globally, continued investment in artificial intelligence, more supportive financial conditions due to tax cuts and declining interest rates, and a slowing but stable labor market. At the same time, we believed returns would be more modest and markets would likely become more volatile given elevated valuations and a later-stage cycle.

Much of that view still holds. Earnings have continued to hold up, with first quarter estimates recently revised higher, and the labor market, while slowing, continues to show resilience, as evidenced by the latest job report coming in better than expected. Investment in artificial intelligence remains strong and is beginning to broaden beyond large technology companies into other areas of the economy. These factors continue to support economic activity and provide a foundation for markets.

At the same time, the outlook has begun to shift in recent weeks. Earlier in the year, much of the focus was on tariffs and policy uncertainty. That focus has now moved toward energy, as the conflict in the Middle East and the resulting supply disruption has renewed inflation pressures. This has also begun to influence interest rate expectations, with the Federal Reserve now balancing a backdrop of moderating growth with renewed inflation pressure, which will likely limit rate cuts this year.

Higher energy prices also have broader implications. While consumer spending was expected to benefit from tax-related tailwinds, that support may be partially or entirely offset by higher fuel costs depending on consumers overall income level.

Despite recent shifts in the inflation outlook and the source of market risk, the broader environment remains consistent with the view we outlined coming into the year. Markets may continue to move higher, but with more modest returns and a less predictable path. While markets often adjust relatively quickly to short-lived disruptions, more prolonged shocks can have a broader impact on both inflation and growth. At this point, markets appear to be leaning toward a more contained outcome, though that view will likely be tested if disruptions persist.

For long-term investors, periods like this tend to reinforce the importance of staying disciplined, maintaining diversification, and focusing on longer-term objectives.

If you have questions, or would value a conversation, please reach out to us.

0 Comments