Old age is like everything else. To make a success of it, you’ve got to start young.

Theodore Roosevelt

When it comes to finances, it’s becoming harder and harder for young people to focus on their financial well-being beyond making ends meet. Let’s look at some reasons why and follow up with how younger generations can approach the situation they are in.

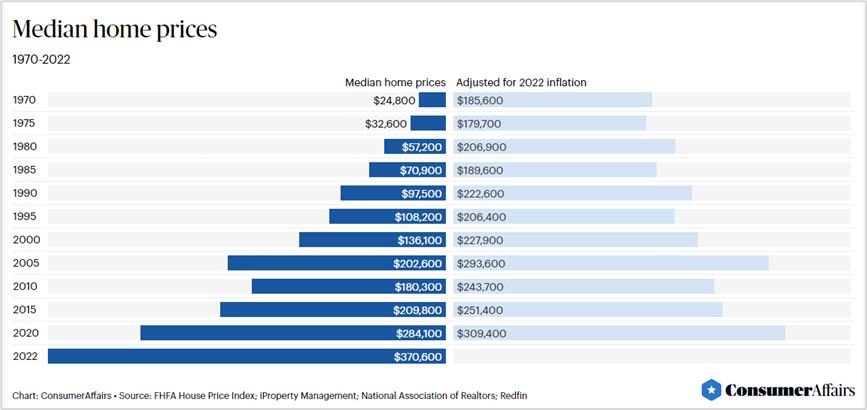

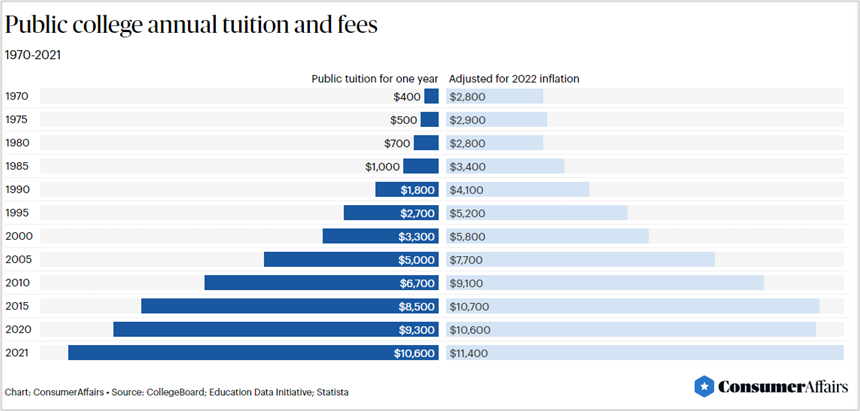

Yes, wages have increased from one generation to the next on a dollar basis. However, it can be challenging to understand the more important measure— purchasing power. According to a Consumer Affairs report, the national Consumer Price Index (CPI) has risen over 500% from 1970 to 2022. During that same time, wages have only increased by 80%. To say it another way, Gen Zers’ money has 86% less buying power than Baby Boomers’ did at the same age.

Some of the most striking examples are in home buying and education costs. Even on an inflation adjusted basis, median home prices have nearly doubled the 1970’s prices and education has risen four times its 1970’s prices. This leaves no question as to why there is more debt for younger generations on average.

As a Millennial, this information blows my mind! And while building wealth is harder, it’s not impossible. The key is discipline. While there is a lot working against us, it’s important to take advantage where we can of the systems in place.

- Prioritize a Plan.The simple act of having a prioritized plan for what you want to achieve can be powerful. Think about how you can best leverage your career to achieve your goals. What would the payoff be to complete additional training or get a master’s degree? Are there employers and projects that would reflect more favorably on your resume for future job opportunities?

- Apply for Scholarships. There are thousands of scholarships out there, offered by a variety of resources and organizations. Scholarships are gifts and don’t need to be repaid. Start your research and detective work early to help with free money for college or career school.

- Take Full Advantage of Employee Benefits. Dig into your company’s benefit package, reviewing each open enrollment period to understand new benefits offered and what changes you may need to make. More employers are offering educational assistance programs to help with tuition reimbursement. In addition, wellness programs through your medical insurance can often include gym memberships, wellness incentives and mental health resources.

- Raise Your Goals. Put a portion of every pay raise toward your goals, rather than using all to increase lifestyle. Make sure your savings rate keeps up with inflation, too ($100/month will seem like a tiny contribution 10 years from now but can make a big difference in a high yield savings account!).

- New Homebuyer Programs. Familiarize yourself with programs available for first-time homebuyers. Depending on your situation, you may be eligible for a forgivable loan, reduced interest rates, or help with closing costs.

- Start a Roth IRA. One of the primary advantages of a Roth IRA is that qualified withdrawals in retirement are tax-free, meaning both your contributions and any investment gains can be withdrawn without incurring federal income taxes. Millennials should start investing early and take advantage of the compounding effect.

While the road to wealth for millennials and younger generations may be different than the generations before, working with a financial planner can help navigate the ever-changing financial landscape and new opportunities.

If this article spurs a question about your financial situation, reach out to your financial planner. If you’d like to learn more about working with our team, schedule an introductory call.

0 Comments