As we provide our financial perspective on the conflict in the Middle East, we are mindful that events like this have human consequences beyond market implications, and our thoughts are with those whose lives and families are affected.

Recent geopolitical developments in the Middle East have understandably raised questions about how markets may respond. Rather than speculate, our approach is to look to institutional research and long-term data to provide perspective.

The historical pattern reveals:

- Geopolitical shocks often trigger short-term volatility.

- Equity markets typically experience moderate drawdowns, not prolonged declines.

- Markets tend to reprice quickly and stabilize, often before conflicts are resolved.

- Longer-term returns are driven far more by economic fundamentals than by isolated geopolitical events.

What does decades of research from major firms including LPL Financial, JPMorgan Chase, and others tell us about how markets react to geopolitical conflict? Here are several of the findings:

1. Short-term Volatility Is Normal

An analysis of more than two dozen geopolitical shocks since World War II found:

- The S&P 500 declined 4.6% on average at its trough following geopolitical events.

- The average time to market bottom was approximately 19 days.

- The average time to recover to prior levels was approximately 40 days.

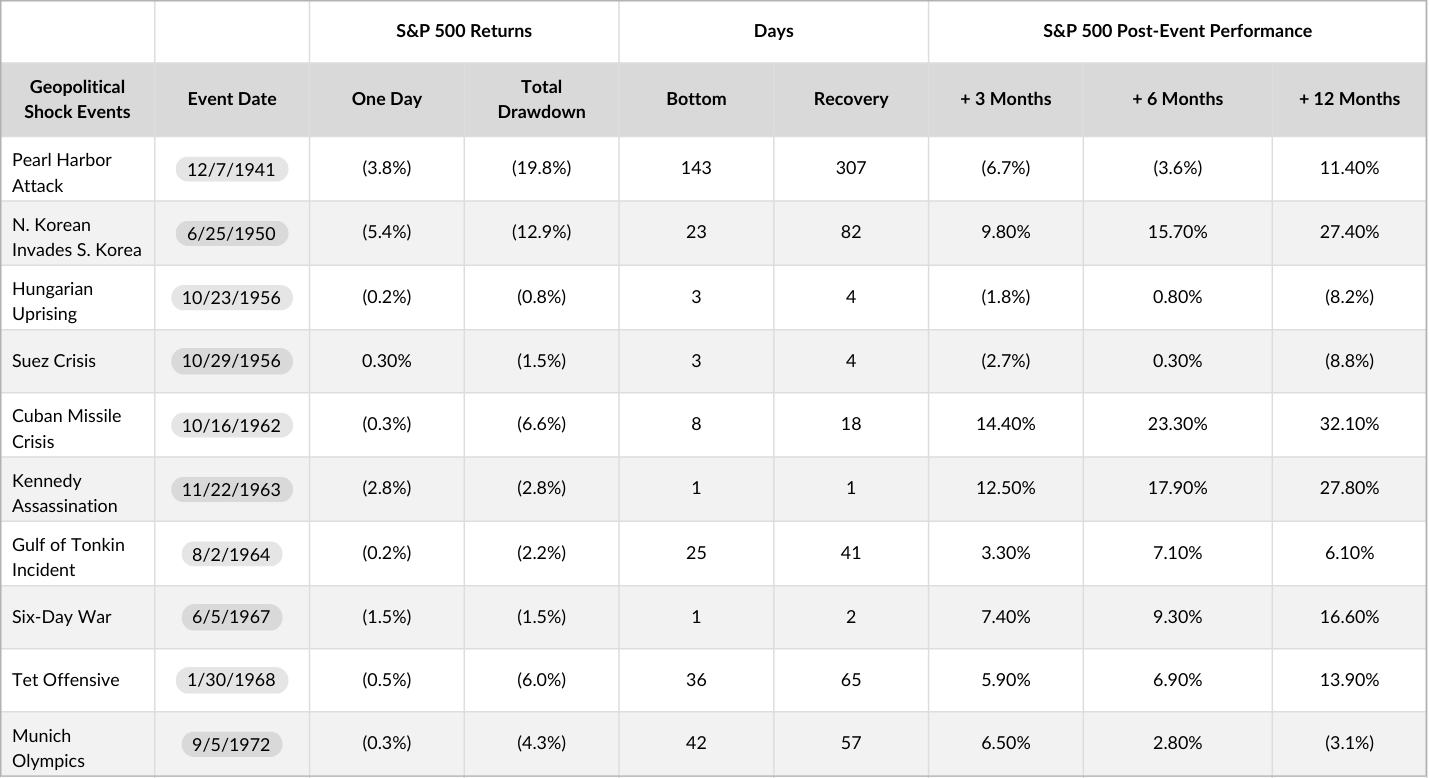

Stocks Have Historically Been Resilient Following Geopolitical Shocks

S&P 500 Responses to Select Geopolitical Events Since World War II (Click on image to view full chart)

Sources: LPL Research, Bloomberg, Factset, S&P Down Jones Indices, CFRA, “Stocks Have Historically Been Resilient Following Geopolitical Shocks,” 2025.

These findings reinforce a consistent pattern: markets react quickly to uncertainty but often stabilize once the scope of the event becomes clearer.

2. Markets Often Begin Recovering Before Conflicts End

Importantly, markets are forward-looking.

Research indicates that when geopolitical events do not coincide with recessionary conditions, equity returns over 3-, 6-, and 12-month horizons tend to align with long-term averages.

In many historical cases, markets began recovering before conflicts were formally resolved, reflecting the market’s tendency to discount expected outcomes in advance.

A Historical Example: The Gulf War (1990–1991)

In August 1990, Iraq invaded Kuwait. Oil prices surged. Markets reacted quickly.

The S&P 500 fell approximately 17% from peak to trough amid fears of prolonged Middle East conflict and energy disruption. Yet once military action began in January 1991 and investors gained clarity around the likely scope of the conflict, markets began recovering — even before the war formally ended.

By the end of 1991, the S&P 500 had delivered strong positive returns for the year.

Markets tend to price uncertainty rapidly. When worst-case outcomes fail to materialize, recoveries often begin sooner than expected.

Equity Markets Have Historically Powered Through Geopolitical Events

Sources: Capital Group, Refinitiv Datastream, Standard & Poor’s. Chart shown on a logarithmic scale. Index levels reflect price returns, and do not include the impact of dividends. As of January 31, 2022.

3. Oil Shocks Have Historically Been the Main Outlier

The most significant geopolitical-related drawdowns in modern market history were tied to energy supply disruptions, most notably the 1973 oil embargo.

During that period, oil prices surged dramatically, inflation accelerated, and economic growth deteriorated — leading to a much deeper and more prolonged market decline.

However, structural conditions today differ materially from the 1970s:

- The U.S. is significantly less dependent on foreign oil imports than in prior decades.

- Domestic production capacity is substantially higher.

- Global energy supply chains are more diversified.

And while oil prices can spike temporarily during Middle East tensions, sustained economic impact typically requires prolonged and material supply disruption.

This distinction matters.

4. Emerging Markets: Commodity Exporters, but Often Energy Importers

Emerging markets are often thought of as commodity-driven economies—and many are significant exporters of copper, gold, silver, agricultural goods, and rare earth materials.

However, a number of these same economies are net importers of energy and oil, making them vulnerable to rising energy prices even if they benefit from strength in other commodities.

Institutional research shows that energy-import-dependent emerging markets can experience higher inflationary pressure, currency volatility, and growth headwinds when oil prices spike. Outcomes can vary significantly by country, reinforcing the importance of careful country selection, broad diversification, and disciplined portfolio construction within emerging markets allocations.

5. Longer-term Market Outcomes Have Historically Been Positive

Across the majority of geopolitical shock events studied since World War II, the S&P 500 has delivered positive returns over subsequent 12-month and multi-year periods, provided broader economic fundamentals remained stable.

The key driver over time has not been geopolitical headlines, but rather:

- Corporate earnings growth

- Economic expansion

- Interest rate policy

- Valuations

What This Means for Long-term Investors

History does not suggest that geopolitical events should be ignored. They can and do cause volatility.

But history also shows:

- Most geopolitical shocks have resulted in temporary drawdowns, not structural bear markets.

- Markets typically begin to recover once uncertainty begins to clear.

- Long-term investment outcomes are driven by economic fundamentals, not isolated geopolitical events.

This historical perspective reinforces why disciplined asset allocation, diversification, and periodic rebalancing remain central to long-term portfolio strategy.

Short-term volatility is uncomfortable, but it is not unusual. And it has not historically derailed long-term wealth creation.

Reach Out If You Have Questions

While geopolitical events can create short-term volatility, our investment approach is built to navigate evolving conditions through strategic asset allocation, diversification, and ongoing oversight.

We’re not expecting any changes to our economic and market outlook but will continue to monitor developments related to this conflict and will make adjustments to portfolios aligned with our clients’ goals.

If you have questions or would simply value a conversation, we are here.

Sources:

Goldman Sachs, “Heightened Geopolitical Risks,” 2024.

JP Morgan Chase, “How do geopolitical shocks impact markets?,” 2025.

LPL Research, “Israel-Iran Conflict: Stocks Face Another Geopolitical Test,” 2025.

Capital Group, Market Volatility Insights Article, 2022.

0 Comments