Updated June 2026

In our previous articles in this series, we discussed what happens when you inherit assets and how inherited retirement accounts come with their own set of tax rules and distribution requirements.

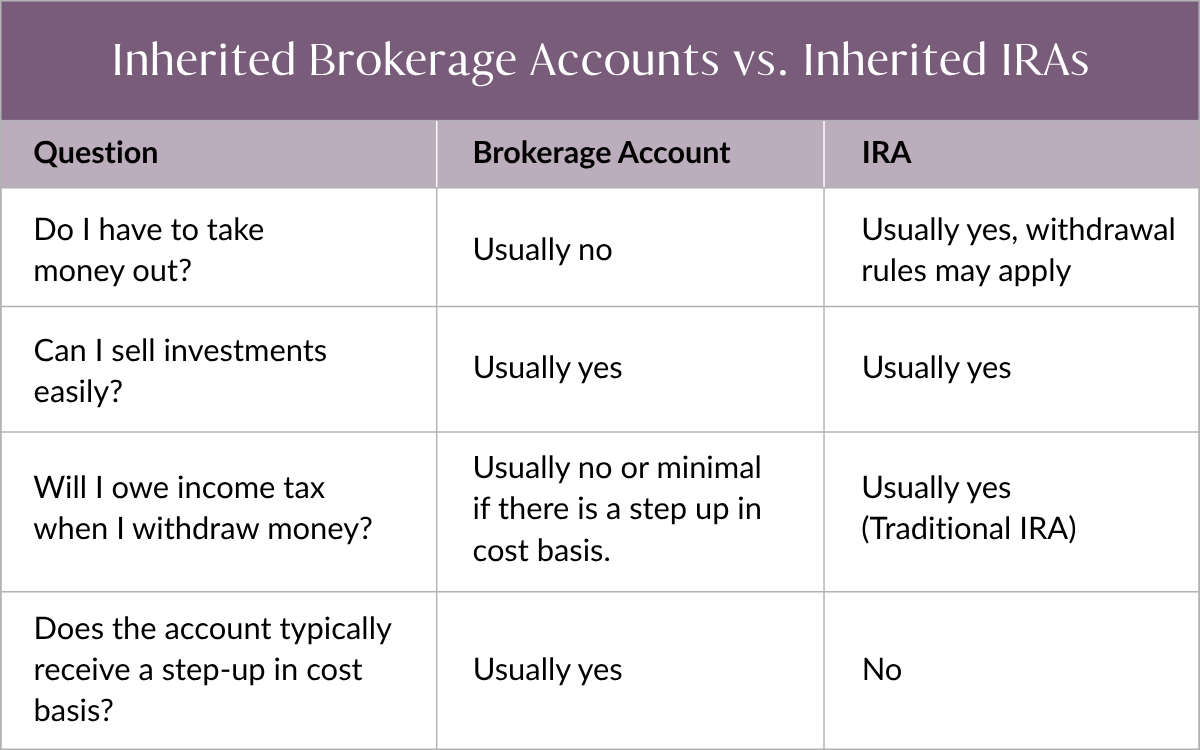

Inherited brokerage accounts often have less complexity.

In many cases, inheriting a brokerage account gives you more flexibility than inheriting an IRA or other qualified retirement accounts. There are typically no required distributions or 10-year withdrawal rules. Rather they often have a valuable tax benefit known as a step-up in cost basis.

But before focusing on the account itself, it can be helpful to take a step back and consider the bigger picture.

Key Takeaways

- Inherited brokerage accounts generally offer more flexibility than inherited retirement accounts.

- A step-up in cost basis may significantly reduce future capital gains taxes.

- You may have the flexibility to sell, diversify, or reposition inherited investments.

- Don’t assume you should immediately liquidate the account—consider taxes, markets, and your goals first.

- A thoughtful plan can help turn an inheritance into a lasting financial resource.

Reframe Inheritance as a Financial Resource

An inheritance is more than a collection of investments. It represents a financial legacy built over a lifetime. As a steward of this financial resource, it can potentially support important goals, create new opportunities, or strengthen your long-term financial security. Understanding how these assets fit into your overall financial plan may be just as important as understanding the investments themselves.

The decisions you make after inheriting a brokerage account can affect your taxes, investment strategy, and long-term financial goals for years to come. Ask yourself:

- What purpose should this money serve?

- Did the person I inherited the money from express a desire for how it is used?

- Do I need current income, long-term growth, or flexibility?

- How does this inheritance fit alongside my existing savings and investments?

- Are there tax planning opportunities I should consider?

- Does this inheritance change my long-term financial goals?

The Step-Up in Cost Basis Advantage

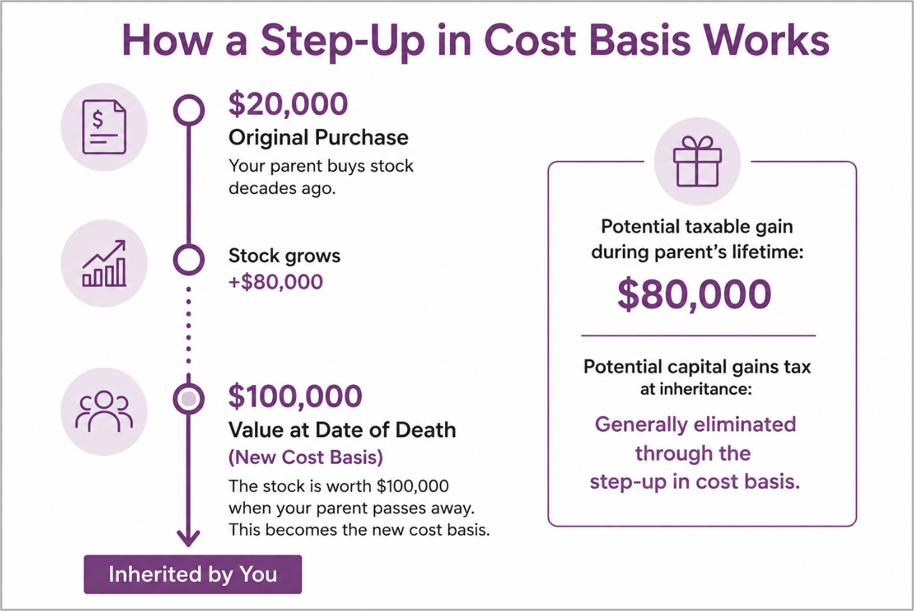

One of the most significant benefits of inheriting a taxable brokerage account is the potential step-up in cost basis.

In general, when someone inherits investments held in a brokerage account, the cost basis of those assets is adjusted to their fair market value as of the owner’s date of death (or an alternate valuation date if elected by the estate).

Cost basis is generally what the original owner paid for an investment. When investments are sold, capital gain taxes are calculated based on the difference between the original purchase price and the cost basis.

A step-up in cost basis resets that starting point.

For example, imagine your parent purchased shares of stock decades ago for $20,000, and those shares were worth $100,000 when they passed away. If you inherit the shares, your cost basis would generally be reset to $100,000 rather than maintaining the original $20,000 purchase price.

As a result, the $80,000 of appreciation that occurred during your parent’s lifetime may never be subject to capital gains tax.

Note: Step-up rules vary in certain situations involving trusts, jointly owned property, and community versus non-community property states. This example is for illustrative purposes only.

What This Means for You

The step-up in cost basis can provide flexibility that might otherwise create a substantial tax burden.

Depending on your circumstances, you may be able to:

- Sell inherited investments with little or no immediate capital gains tax

- Reallocate investments to better align with your risk tolerance

- Diversify a concentrated stock position

- Build a portfolio that reflects your own goals and timeline

- Use a portion of the assets for other priorities, such as paying down debt, funding education, supporting charitable causes, or strengthening your retirement plan

But Don’t Rush to Liquidate Everything

Many inheritors assume they should immediately sell everything and move the money to cash. Sometimes that makes sense. Often it doesn’t.

Before making changes, consider:

Market Conditions

If markets have declined significantly since the date of death, selling may create a different tax result than expected. Likewise, if investments have appreciated since you inherited them, capital gains could already exist.

Future Tax Consequences

While the step-up in cost basis can reduce tax on gains accumulated during the original owner’s lifetime, future growth remains taxable.

Your Investment Strategy

The inherited portfolio may—or may not—be appropriate for your situation.

Ask yourself whether you would purchase these same investments if you were starting from scratch today. If not, it may make sense to gradually reposition the portfolio.

Emotional Decision-Making

An inheritance often arrives during a period of grief and transition. Unless there’s an urgent need, allowing yourself time to evaluate your options can help prevent decisions you’ll later revisit.

Bottom line: brokerage accounts are often the most flexible inherited investment asset because they generally receive a step-up in cost basis and aren’t subject to the distribution rules that apply to inherited retirement accounts.

Final Thoughts

Inherited brokerage accounts can offer both flexibility and tax advantages, particularly when a step-up in cost basis applies.

Before making major changes, take time to understand the investments you’ve inherited, the tax implications of your options, and how these assets fit within your overall financial plan.

If you’ve recently inherited investment assets, working with a CFP® professional and tax advisor can help you evaluate your choices and make informed decisions about what’s next.

Frequently Asked Questions

Do I pay taxes when I inherit a brokerage account? Generally, no. Simply inheriting a brokerage account does not typically create an immediate income tax liability. Taxes may apply later if you sell investments that have appreciated since the date of inheritance.

Should I sell everything right away? Not necessarily. While the step-up in basis often provides flexibility to sell investments with minimal tax consequences, the best decision depends on your financial goals, investment strategy, and overall plan.

What is cost basis? Cost basis is the value used to calculate capital gains or losses when an investment is sold. For inherited brokerage accounts, the basis is generally adjusted to the asset’s fair market value on the date of the original owner’s death.

Do inherited brokerage accounts require withdrawals? No. Unlike many inherited retirement accounts, inherited brokerage accounts generally do not have required minimum distributions or mandatory withdrawal schedules.

Can I keep the investments instead of selling them? Yes. You can generally continue holding inherited investments if they align with your goals and risk tolerance. The decision should be based on your overall financial plan rather than solely on tax considerations.

Dear all

We have a trust and name my son as inherited person of my brokerage account after my death. Will my son receive the prorated stocks prices after I die while my wife is still alive?

Thank you

Hello Joseph! Thanks for inquiring. If you’d like to discuss your question with one of our financial planners, we offer Free Financial Planning Day on the 4th Wednesday of every month. To sign up for a 30-minute session, register for in-person or online meeting via the link on our Community & Events page.

I have two adult children to whom I will leave my estate to. Some things have been taken care by a will the problem are my investments. Brokerage, ROTH and Trad. IRA.. I am trying to protect my daughter from herself so to that end I am leaving everything to my son with the understanding that the brokerage account will be under his name but the monies will be distributed to her on an annual basis, 4% rule. The split comes in at 55/45 son/daughter. Presently his cut will be 880.7K from ROTH and Trad IRA. The brokerage account will also be under his name but doled out to daughter, her cut is at 720.6K mostly from brokerage ~87K from ROTH.

What are the tax implications to my son? Is there a better way? Daughter cannot be trusted with that much money. If given to her today she’ll be broke in 2 years.

Thank you for sharing your situation. Many parents face similar concerns when thinking about how to leave an inheritance in a way that supports their children while also protecting them from potential financial mistakes. We just held an event addressing these and similar issues. Here is a link to a recording of the event we’d encourage you to watch for items to consider.

Because the tax, legal and estate planning implications can vary significantly based on your specific circumstances, you may want to talk with an estate planning attorney and/or a financial planner who can help evaluate strategies that align with your wishes while protecting both children and minimizing unintended consequences.

We invite you to attend one of our upcoming Free Financial Planning Days, where you can have a confidential conversation about your situation with one of our Certified Financial Planners® either in person if you’re in the Portland/Vancouver area or via Zoom.

Learn more and register for a free 30-minute session in August, September or October here.