After the Seahawks’ recent Super Bowl run, and a magical return to the playoffs for the Mariners last season, the Pacific Northwest sports scene is thriving. However, it’s not just the teams and their fans that are celebrating, it’s also the gaming industry.

The Explosion of Legal Sports Betting

Kicking off 2026, there were 39 states, plus the District of Columbia, that allow legal sports betting, including both Washington and Oregon. In Washington, we have tribal-casino-only betting, but across the Columbia River, you also have the option to bet on your mobile device through a state-sanctioned app.

This won’t come as a surprise to those who’ve watched a live sporting event in the last several years. The commercials, sponsorships, and promotions are ubiquitous. While the exact numbers are hard to come by, companies like DraftKings and FanDuel are estimated to have spent over a billion dollars on marketing and advertising in 2025 alone!

So, you might be saying to yourself, “this information is neat, but what does it have to do with financial planning and investing?” For us, it’s about educating clients and our community about the difference between sports betting (i.e., gambling) and investing.

Understanding the difference between the two is not to vilify one and glorify the other, it’s to make sure the distinction is clear, so your saving and spending habits are in alignment with what’s most important to you.

The Key Difference: How Time Works

My favorite way to distinguish the two is by comparing how each is affected by time. If you’re betting on sports, the longer you play, the more likely you are to lose*. This is known as ‘negative expected value’ and is why casinos and sports betting apps pour so much money into keeping you at the table (or on your phone) as long as possible. Contrast this with investing, where the inverse is true. The longer you invest, the greater likelihood of ‘positive expected value’, better known as growing your initial investment.

*Theoretically skilled sports bettors can identify mispriced odds and focus on bets deemed to have positive expected value, but this represents a tiny fraction of sports bettors and sportsbooks can adjust odds or limit/restrict successful bettors.

Why Long-Term Investors Have the Odds on Their Side

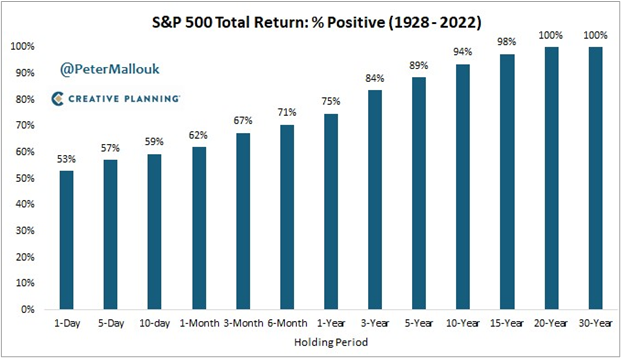

Source: Bloomberg, Crestmont Research, and historical S&P 500 data (1928–present).

As the chart above demonstrates, if you invested in the S&P 500 (an index of America’s largest 500 companies) for just one day, you’ve essentially engaged in a coin flip for whether that investment will rise in value. Increase your holding time to one month, and the historical likelihood of gain increases to over 60%. One year? 75%. 10 years? 94%. Any investor that has stayed invested in the S&P 500 for 20 years or more has never had a negative total return! Past performance never guarantees future results, but the broader lesson remains: disciplined, diversified investing tends to improve outcomes over time, something gambling simply can’t offer.

Now, are there some similarities between sports betting and investing? Of course. Both involve risk and the potential for loss or gain, but the Venn diagram overlap largely ends there.

Investing involves real economic activity–think profits, dividends, productivity growth, etc. With a sports bet there is no real economic activity that drives outcomes, you are simply hoping to outsmart the oddsmakers.

The Reality of Sports Betting

Sports betting markets are structured so that only a small minority of participants consistently win, otherwise they wouldn’t be a successful businesses! Research suggests that only a few percent of bettors are profitable over time, while the overwhelming majority lose money. While this includes the recreational gambler who places a few bets while at the casino with friends, it also includes “problem gamblers”, which are defined as people whose gambling behavior damages their personal life, finances, career, etc. A study cited by Barron’s found that just 5.7% of bettors generate 80% of sportsbook revenue, highlighting how losses are concentrated among a handful of participants, many of whom likely qualify (or self-identify) as “problem gamblers”.

This is why we don’t conflate gambling with investing. When we’re helping clients construct fully diversified portfolios that align with their financial timeline and goals, we can confidently say that one bad call from a referee or an errant gust of wind will not impact their retirement.

Does that mean you need to avoid sports betting at all costs? Of course not! Placing a $10 bet on the Seahawks to win the Super Bowl is vastly different from wagering funds and calling it part of your retirement savings plan.

Why Younger Generations Are More Likely to Blur the Line

A 2024 survey by NerdWallet showed 24% of Gen Z gamblers and 22% of Millennials viewed it as an investment, compared to 10% of Gen X and 3% of Baby Boomers. The same survey also highlighted that Gen Z respondents gambled $1,885 annually, compared to $1,027 for U.S. gamblers overall.

Younger bettors are also much more likely to place these bets on their mobile devices, where gamification can emphasize excitement, frequent action, and immediate feedback. Investing is not entirely immune from these methods—think the ‘meme stock’ and cryptocurrency mania of the COVID pandemic—but in its healthiest form investing emphasizes patience, infrequent trading, and delayed gratification. As finance writer Morgan Housel puts it, “The biggest secret in investing is that average returns sustained for an above-average period of time lead to extraordinary returns.”

Treat Betting as Entertainment—Not a Financial Strategy

If you want to talk to a Financial Planner about how your own savings and retirement planning can align with your long-term goals, sign up for our next Free Financial Planning Day, held via Zoom or in-person on the last Wednesday of each month.

And if you recognize your sports betting is causing significant issues for your finances or relationships, consider reaching out to the problem gambling helpline at 1-800-GAMBLER (1-800-426-2537), available 24/7, free and confidential.

About the Author

Zach Reuter, CFP®, is a CERTIFIED FINANCIAL PLANNER® professional at Johnson Bixby. His work focuses on retirement planning, tax planning strategies, inheritance planning, employee benefits analysis, and college funding strategies for individuals and families. Learn more about Zach.

")

Zach — great breakdown. A few points really landed for me:

• Time is the real separator. Betting punishes you the longer you play; investing rewards you the longer you stay invested.

• Expected value is the whole story. Betting is structurally negative‑EV. Investing is tied to real economic growth and compounding.

• The psychology couldn’t be more different. Betting thrives on immediacy and emotion; investing requires patience and discipline.

• Younger generations are blurring the lines. The stats you shared on Gen Z treating gambling like investing are a real signal that financial literacy needs to catch up with the pace of legalized betting.

• Clear takeaway: Sports betting can be entertainment — but it’s not a wealth‑building strategy.

Thanks for putting this into plain language. It’s a distinction a lot of people need to hear right now.

Doug, thanks for taking the time to read and provide such thoughtful commentary. I’m glad the message resonated for you and I hope others had a similar experience. Keep reading, I’ll be writing again soon! – Zach