The first half of 2026 brought a number of developments that influenced financial markets, including a sharp market decline tied to geopolitical events in March followed by a meaningful recovery during the second quarter. As we reach the year’s midpoint, it’s a good opportunity to look back at what influenced market performance and consider what may shape the months ahead.

Key Takeaways

- A tale of two quarters: a first-quarter decline as conflict in the Middle East disrupted oil supplies and reignited inflation fears, then a meaningful second-quarter recovery as tensions eased and corporate earnings came in strong.

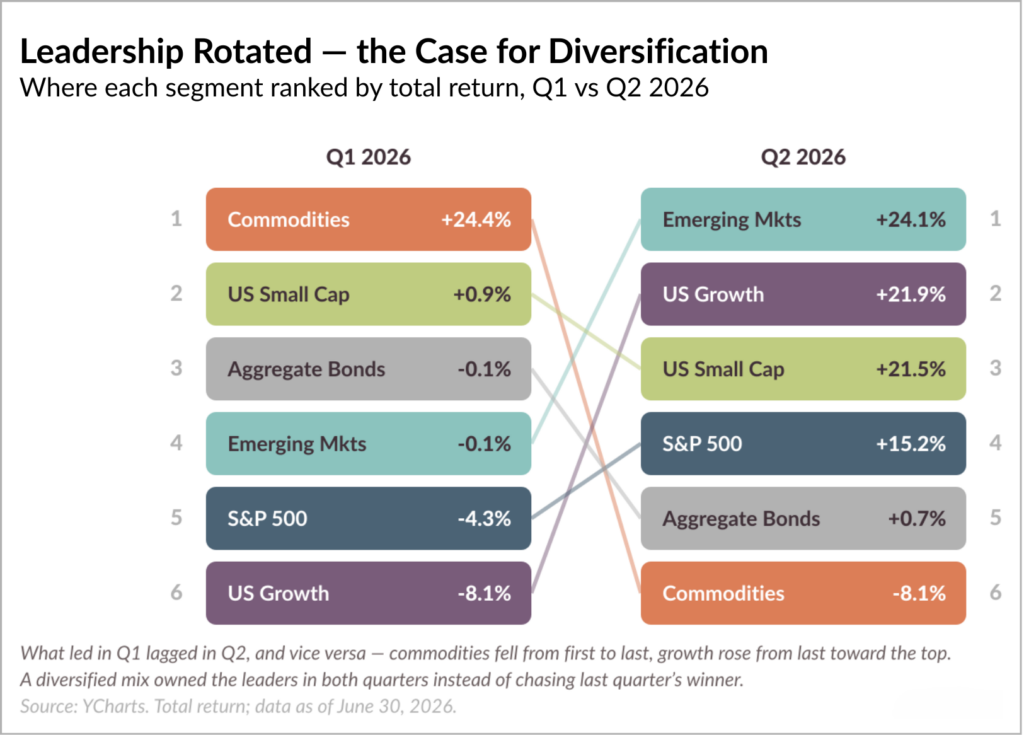

- Broadened market leadership: gains extended well beyond the largest technology stocks to small-cap, mid-cap and international stocks.

- As we look to the second half of the year, there are some positive trends, yet areas to watch that continue to warrant attention. Earnings are solid and energy prices have cooled, but stock valuations are full again and the market’s biggest names still carry a lot of weight, so we continue to expect more modest returns and a bumpier ride than in recent years.

A Difficult Start, a Strong Finish

As we noted in our outlook entering 2026, we expected continued economic growth alongside more modest returns and higher market volatility after several strong years. That volatility arrived early in the year. Markets were rattled when conflict in the Middle East disrupted global energy supplies and effectively closed the Strait of Hormuz, a waterway through which a large share of the world’s oil travels each day. Oil prices spiked, which reignited inflation concerns and led investors to abandon their expectations for Federal Reserve rate cuts. The S&P 500 fell about 4.3% in the first quarter. Even so, there were early signs of resilience beneath the surface. Small-cap stocks held up considerably better than the S&P 500, suggesting that market leadership—or the companies driving overall market performance—was beginning to broaden.

The second quarter was almost a reverse mirror image. As the conflict moved toward a ceasefire and energy flows began to normalize, oil prices reversed sharply, with U.S. crude oil sliding back toward $70 per barrel by the end of June. Falling energy costs eased inflation worries and a wave of strong corporate earnings did the rest. The S&P 500 climbed roughly 15% in the second quarter—its best quarter since 2020—and finished the first half up about 10.2%, reaching an all-time high above 7,600 before easing slightly into quarter-end. The Dow Jones Industrial Average gained about 13% in the second quarter and closed above 52,000 for the first time. The technology-heavy Nasdaq Composite rose nearly 22%, also its best quarter since 2020.

Broadening Leadership and the Value of Diversification

The most encouraging feature of the half was not just how much the market gained, but where those gains came from. After several years in which a small group of very large technology companies drove most of the market’s returns, participation broadened meaningfully across companies of different sizes and regions.

Small-cap stocks led the way. The Russell 2000 surged nearly 22% in the first half—its best start to a year since 1991—and reached a new all-time high, helped by improving fundamentals and the widening reach of AI-related spending. Mid-caps also participated. Historically, broader market participation has often provided a more balanced foundation than periods when returns are driven by only a small number of companies.

International stocks extended the strong run they began in 2025. Emerging market stocks were among the best performers of any major region, up more than 24%, supported by a weaker U.S. dollar and more attractive valuations relative to the U.S., though the strength was uneven, with China lagging. Developed international markets also posted solid high-single-digit gains.

The first half also served as a reminder of why diversification remains an important investment principle. Allocating a portfolio across company sizes, styles, and geographies meant that when the largest technology stocks pulled back in June, other holdings were there to help offset the decline.

The AI Story Broadens Beyond Technology

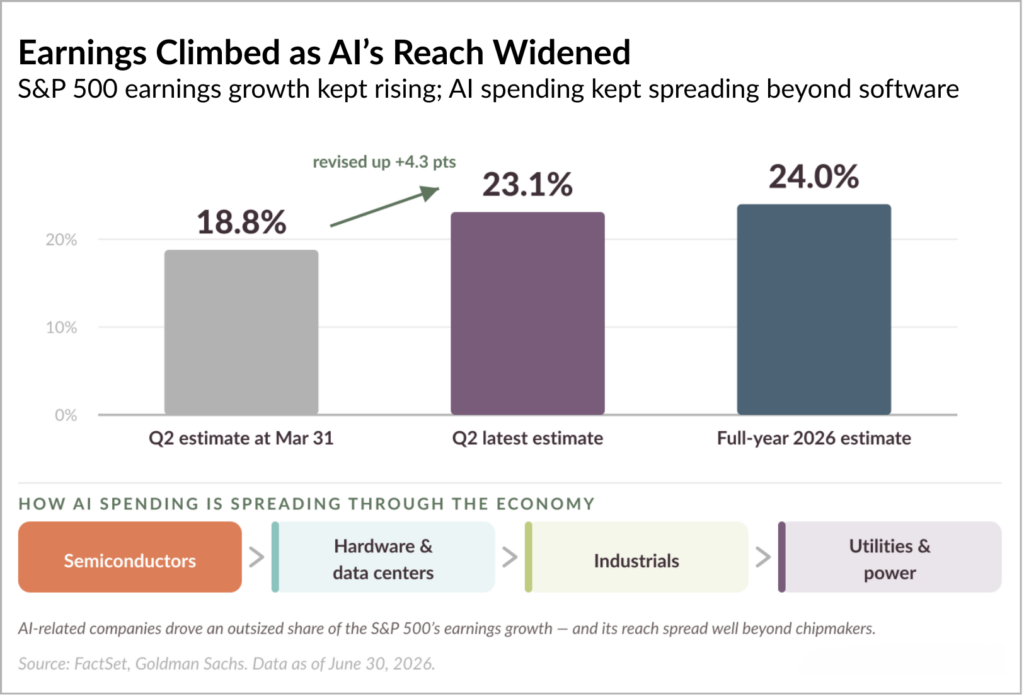

Artificial intelligence remained the market’s dominant theme, but its reach widened. Rather than benefiting only software and internet companies, AI-related spending appears to be contributing to increased activity across multiple sectors of the economy, although the long-term impact remains uncertain. Semiconductor companies were the clearest winners, and industrial and utility companies tied to data centers and rising electricity demand also saw a meaningful lift in orders and earnings—a sign that AI investment is translating into real activity across the broader economy.

Strong corporate earnings were an important contributor to the market’s recovery. S&P 500 companies are on track for roughly 23% earnings growth in the second quarter, up from an estimate closer to 19% when the quarter began, with full-year growth projected near 24% on revenue growth around 11%. Rising earnings, more than anything else, explain how the market was able to look past a genuinely difficult start to the year.

Bonds and Interest Rates

Bonds had a quieter first half. With the early-year disruption in energy prices keeping inflation concerns and interest rates elevated, the broad U.S. investment-grade bond market finished roughly flat and modestly trailed cash. The 10-year Treasury yield hovered around 4.4% at mid-year, and shorter-term bonds generally held up better than longer-term ones.

The first half also highlighted the role high-quality bonds can play within a diversified portfolio. During the turbulent first quarter, high-quality bonds generally helped provide relative stability and income during a period of heightened market volatility. With energy prices now retreating and inflation pressures easing, the outlook for bonds in the second half looks more constructive than it did a few months ago. One related note: gold gave back a good portion of its strong 2025 run during the second quarter, as steadier markets reduced demand for safe havens.

Looking Ahead: Optimistic, but Disciplined

Several forces should continue to support markets in the second half of 2026. Corporate earnings remain strong and are still being revised higher. Energy prices have fallen sharply from their spring peaks, easing pressure on both consumers and inflation. With that pressure fading, the Federal Reserve has more room to consider rate cuts later this year, which would be supportive of both stocks and bonds.

We balance that optimism with a few cautions.

- After the market’s strong recovery, U.S. stock valuations have moved back toward historically elevated levels. While that does not determine short-term returns, it can mean future market performance depends more heavily on continued earnings growth and economic conditions.

- Index concentration remains a concern because a handful of the largest companies still account for an outsized share of the market. It is encouraging that market participation has broadened recently, with gains extending beyond the largest technology companies.

Continued stability in the Middle East remains important for energy markets and global supply chains. Inflation continues to move in a positive direction, though it remains above the Federal Reserve’s long-term target. In addition, as the midterm elections approach, markets may continue to respond to political and policy developments. One development during the quarter was the Supreme Court’s decision striking down much of the administration’s tariff program, which removed one source of uncertainty that markets had been monitoring.

While no one can predict how markets will behave over the coming months, the first half of the year served as another reminder that periods of uncertainty are a normal part of investing. Maintaining a diversified portfolio, rebalancing thoughtfully, and keeping your investment strategy aligned with your long-term goals remain some of the most effective ways to navigate changing market conditions.

If you have questions about the markets, your portfolio, or how any of this fits into your broader financial plan, please reach out to your financial planner. We are always glad to connect.

0 Comments