Financial markets finished in similar fashion to how they started the year — in rally mode. After a difficult 2022 and broad expectations of a recession occurring at some point in 2023, equity and fixed income markets finished the year with solid returns, which was a welcome surprise. And while returns largely exceeded subdued expectations last year, markets remain just below the record highs set at the end of 2021.

This raises the question, can markets maintain their positive momentum to new highs in 2024?

Equity and Fixed Income Markets

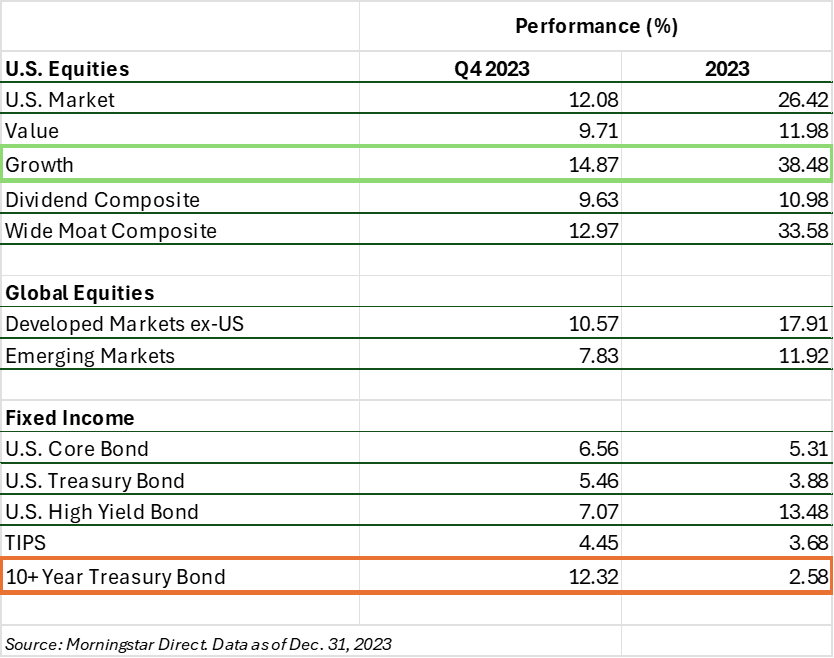

All asset classes appreciated considerably in the fourth quarter of 2023. Leading up to the fourth quarter Large Cap Growth Stocks, led primarily by the largest seven technology companies, now known as the “Magnificent 7”, was where much of last year’s returns were concentrated. See high and low year-end gains in the chart below.

2023 Revisited

While markets finished with positive momentum and broadly exceeded return expectations in 2023, there was significant volatility throughout the year. After raising rates by over 4% in 2022 to quell high inflation, the Federal Reserve continued raising rates to almost 5.5% in 2023. This rapid increase in interest rates led to five bank failures beginning in March and a significant selloff in equity markets. While the Magnificent 7 technology stocks rebounded from their selloff in 2022, high interest rates, a debt ceiling showdown and continued geopolitical tension kept recession concerns elevated, and weighed on most other equity returns for much of the year.

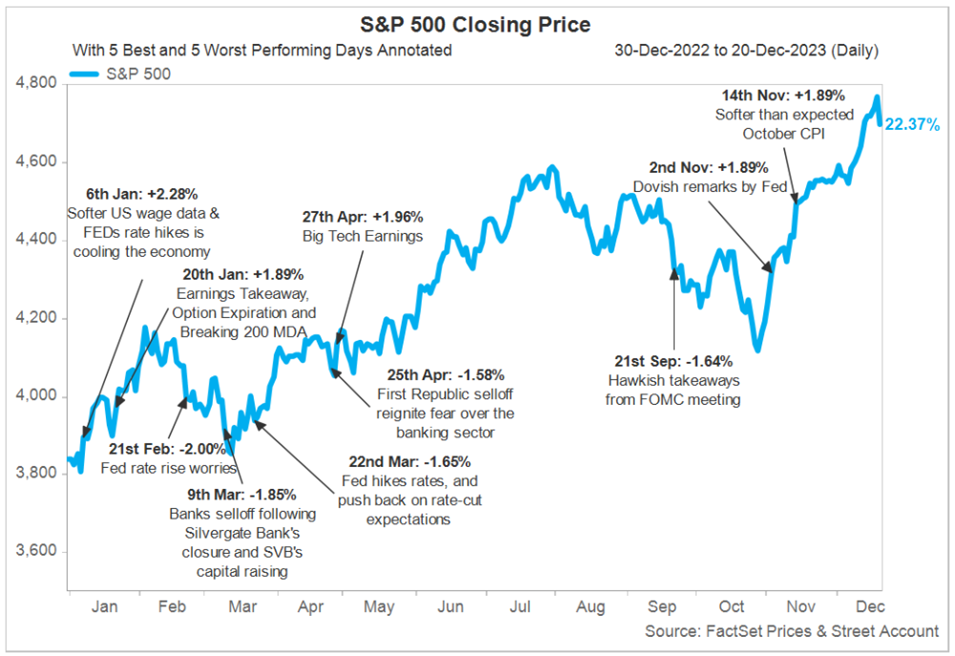

The chart below references the five best and worst performing days of 2023 for the S& P 500. With market volatility, we saw periods when the market was up 2% and down 2% many times throughout the year.

Despite these headwinds and volatility, the overall economy performed quite well in 2023, with GDP expanding almost 3%. Additionally, inflation continued to come down faster than expected starting at 6.4% in January and finishing the year at 3.4% as measured by the Consumer Price Index (CPI).

Finally, unemployment remained low throughout 2023 ending the year with an unemployment rate of 3.7%. Wage gains and the number of job openings did decrease throughout 2023, indicating a more balanced labor market.

Throughout last year, these evolving factors led to the Federal Reserve signaling they were most likely done raising interest rates for now and helped change most economists view from one of expecting a recession in the near term to one of a soft landing and continued economic growth in 2024.

2024, Cash May Not Be King

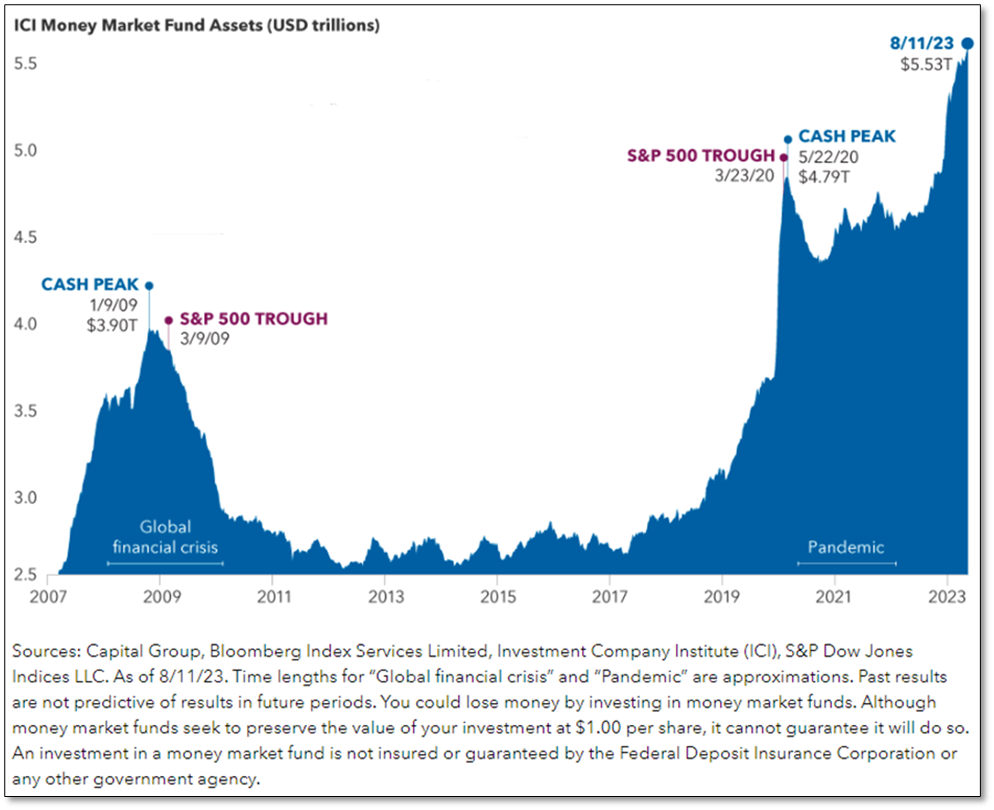

Looking back, 2023 may be celebrated as the year where almost risk-free returns became available. One of the benefits of higher interest rates was the ability to earn 5% or more investing in “risk-free” Treasury bills and notes. The benefit of buying these instruments is there are no transaction costs, and if held to maturity, your return is known and guaranteed by the full faith and credit of the U.S. Treasury. Certificate of Deposit (CDs) and Money Market rates also increased throughout the year.

As short-term rates increased, many investors have enjoyed and taken full advantage of these higher yields. One example is the increased deposits flowing into Money Market Funds as the chart below illustrates:

What’s the Risk?

The biggest risk to holding any of these instruments is known as reinvestment risk. Reinvestment risk is the possibility that you will have to reinvest the proceeds from a matured Treasury bill, note, or CD at a rate lower than your current rate.

While the Federal Reserve was raising interest rates in 2023, reinvestment risk was less of a concern as Treasury holdings matured and needed to be redeployed. Going forward, however, rates are largely expected to decrease throughout the year, with the Federal Reserve projecting three rate cuts by the end of 2024. As a result, now may be a good time to evaluate short-term Treasurys and other cash-like holdings for reinvestment elsewhere for the potential of better long-term returns.

Return to Normal

While 2023 was a year of transition from rising inflation to falling inflation and higher interest rates to falling interest rates, 2024 may be the first year since the pandemic that could be characterized as a return to normal.

So, what is normal?

First and foremost, normal means inflation continues trending toward the Federal Reserve’s long-term target of 2%. This could be helped by housing inflation beginning to trend down modestly in 2024.

Second, the Federal Reserve gradually reduces interest rates toward their longer-term projection of 2.50%. This is well above the 0% rates seen during the pandemic and Great Financial Crisis.

Third is that while GDP growth is expected to slow in 2024, the expectation is that a recession will be avoided, and GDP growth will be more in line with longer term average growth rates.

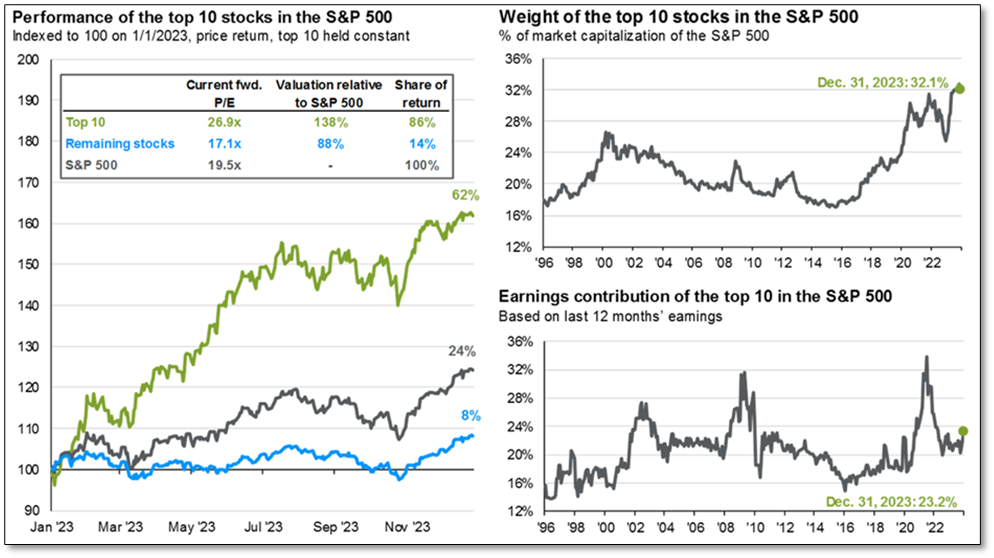

Finally, the following chart shows that much of 2023 market returns were concentrated in the largest 10 stocks in the S&P 500. A return to normal would see this performance broaden out in 2024, potentially rewarding more diversified portfolios.

Normal also means there will continue to be volatility and unexpected events throughout the year. According to a study by Capital Group, investors can expect market declines of over 5% about three times per year and a decline of 10% about once each year.

A Presidential election in the U.S. and geopolitical tensions around the world could be catalysts for some of these potential market events. However, as 2023 illustrated, over time financial markets have rewarded patient and disciplined investors who have a long-term plan in place.

We look forward to partnering with you to help achieve your long-term investing goals in 2024, and beyond.

0 Comments