Original article published in May 2023. Updated October 2025.

Gold has always captivated humans—not just for its beauty, but for its enduring value. Even in our modern financial system, it remains one of the oldest and most trusted stores of wealth. While some investors dismiss it as a relic, gold continues to be a focal point for those seeking stability and diversification, especially as markets navigate persistent inflation, rising interest rates, and global uncertainty.

Why Gold Continues to Rally

Over the past two years, gold has surged to new all-time highs, drawing attention from central banks, institutional investors, and individuals alike. Higher interest rates typically weigh on non-dividend paying assets like gold, yet prices climbed despite this headwind. So, what’s driving the renewed appeal?

In 2024 alone, central banks purchased over 1,000 metric tons of gold, marking the third consecutive year of record buying. This surge reflects concerns about inflation, geopolitical tensions, and the need to diversify reserves beyond traditional currencies. Central banks are using gold not only as a hedge against price instability but also as a safeguard against broader financial and geopolitical risks.

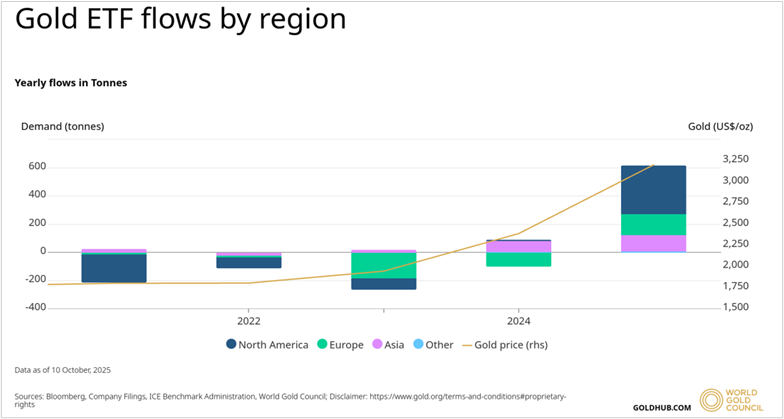

Investor demand has also rebounded. After a period of outflows from gold ETFs and mutual funds, the second half of 2024 saw strong inflows, particularly from retail investors and funds seeking safe-haven assets.

At the same time, global supply increased only modestly, meaning demand pressures continued to push prices upward. Even more compelling, gold’s performance in 2024 rivaled equities: its U.S. dollar price rose roughly 25%–27%, matching or slightly outpacing the S&P 500’s total return. Into 2025, gold continues to hold momentum while equities have shown greater volatility, reinforcing its role as a stabilizing asset.

The Not So Shiny Side of Gold

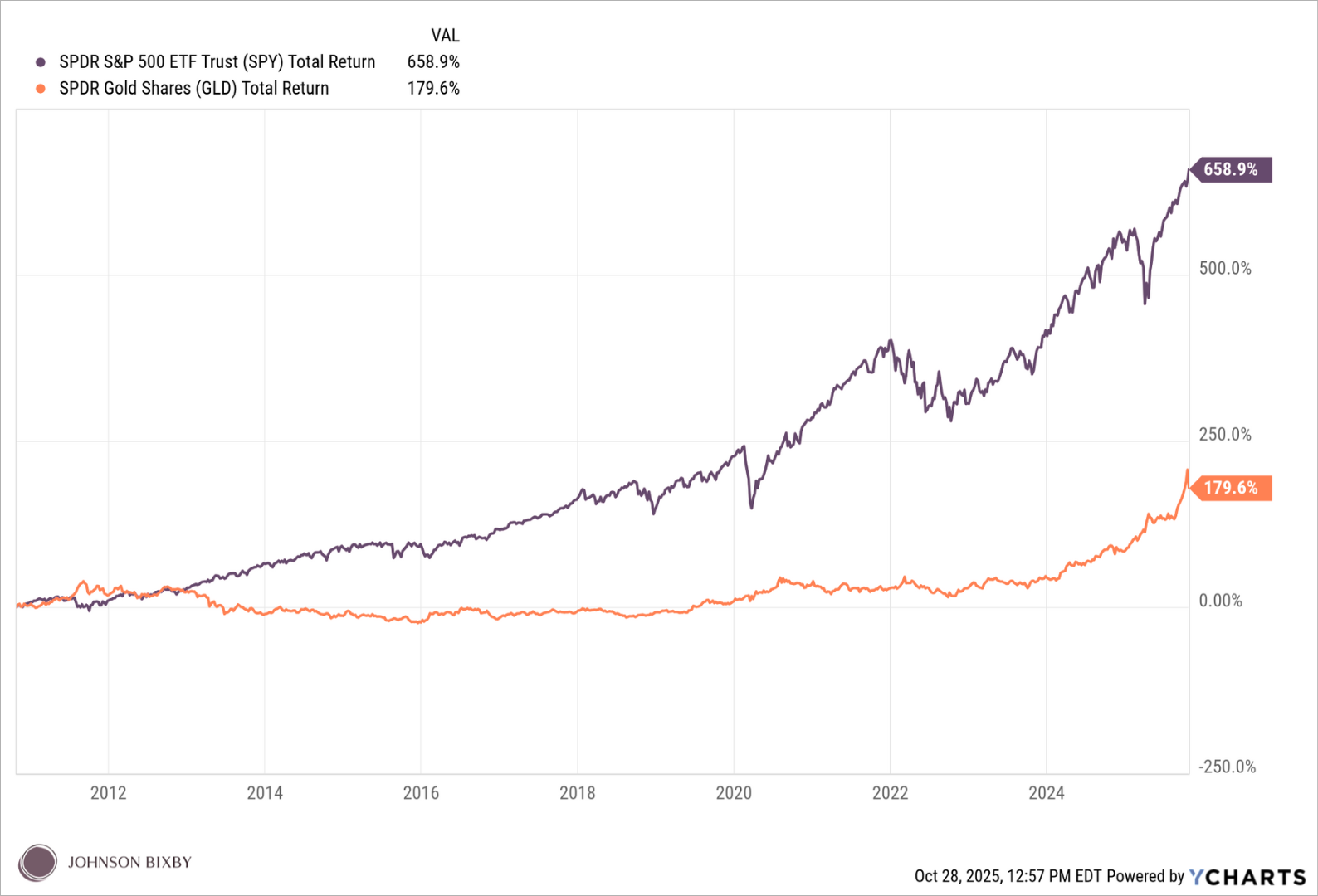

Despite these attractions, gold is not without drawbacks, which explains why opinions among financial professionals vary. Unlike stocks or bonds, gold does not generate income. With no dividend or interest payments, it’s challenging to calculate fair value based on expected cash flows. Warren Buffett famously pointed out that investing in commodities is fundamentally different from investing in productive assets: “The commodity itself isn’t going to do anything for you … it is an entirely different game to buy a lump of something and hope that somebody else pays you more.” As a result, gold can underperform stocks over long stretches if economic fundamentals are strong and corporate profits are growing. The chart below compares the returns of the S&P 500 to Gold over the past 15 years:

Owning physical gold also has practical considerations. Bars and coins must be securely stored and insured, which can add costs over time. Even investing in gold through ETFs or mutual funds carries management fees. Moreover, gold is often thought of as a hedge against financial crises, but if it’s held in paper form, investors could still face liquidity challenges in a systemic event, as seen during the 2023 regional bank failures.

The Case for Gold

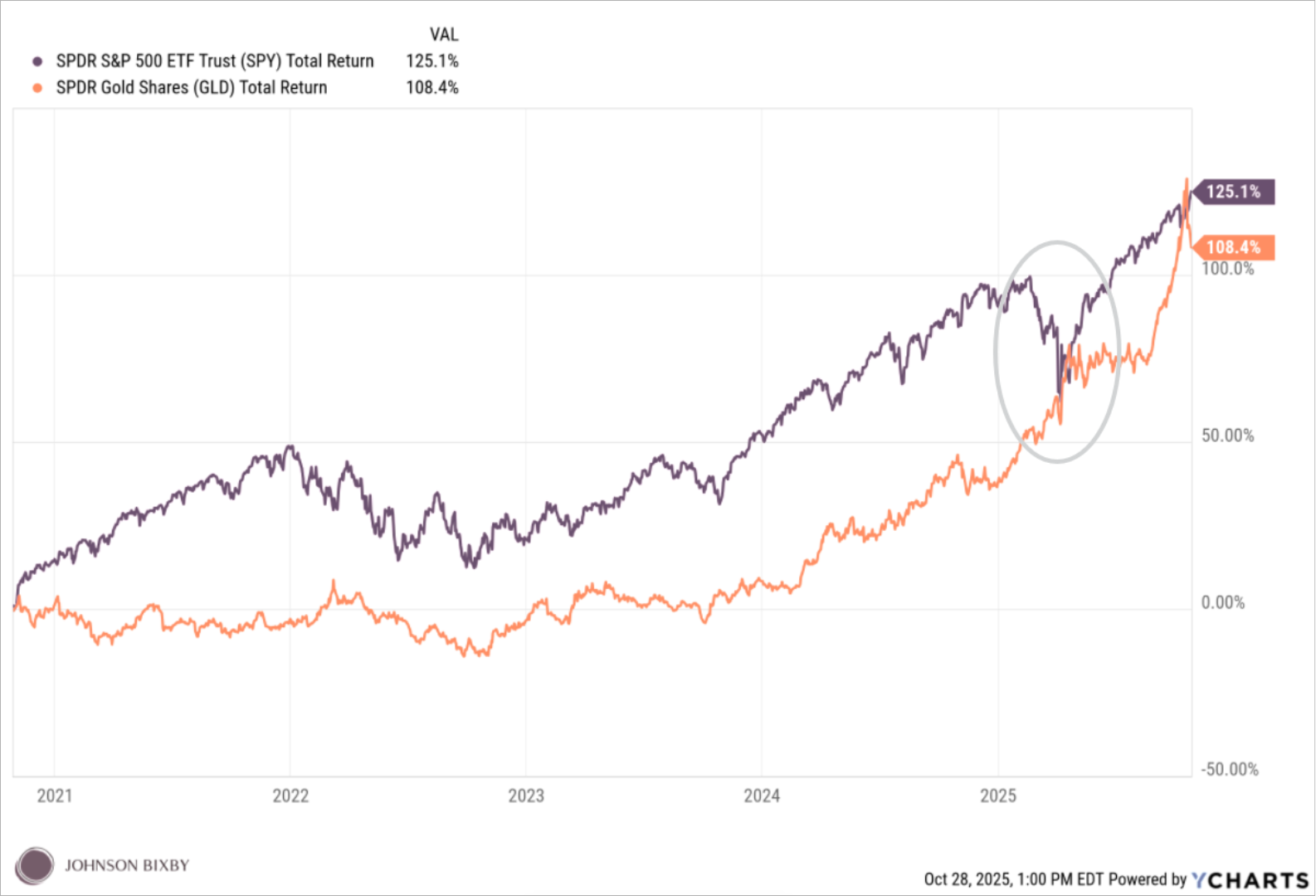

Yet there are positive arguments for including gold in a diversified portfolio. For one, gold can reduce portfolio volatility and act as a stabilizer during periods of economic stress. Historically, portfolios with a modest allocation to gold have experienced smaller drawdowns and more consistent risk-adjusted returns. The chart below compares the returns of the S&P 500 to gold over the past 5 years and shows that gold returns truly shined when concerns around tariffs were at their peak:

Gold may also serve as a hedge against inflation and economic uncertainty. While its reputation as an inflation fighter stems from the 1970s—when gold provided dramatic real returns during a period of double-digit inflation—its more recent behavior suggests it is also effective as a “confidence hedge.” Even as inflation has moderated from post-pandemic peaks, gold prices have remained elevated, reflecting investor concern over the long-term stability of currencies and the fiscal health of governments.

Another factor is diversification. Nobel laureate Harry Markowitz described diversification as “the only free lunch in investing.” Gold’s low correlation with stocks and bonds makes it a unique tool for managing risk, particularly in volatile or uncertain markets. Beyond gold, some investors look at the broader commodities and real assets complex—including silver, energy, industrial metals, and real estate—as complementary ways to enhance portfolio resilience. These assets tend to respond differently to inflation, interest rates, and geopolitical events than traditional financial assets. By thoughtfully combining gold with other commodities and real assets, investors can potentially reduce volatility, hedge against inflation, and add an additional layer of diversification that pure equities and bonds may not provide.

How to Invest in Gold

There are several ways to invest in gold, each with trade-offs. Physical ownership—through coins or bullion—provides direct possession but requires secure storage and insurance. Exchange-traded funds (ETFs) and mutual funds offer easier access and liquidity but involve management fees and do not provide physical control. Gold mining stocks present the potential for additional upside, as their value is linked both to gold prices and operational performance, though they come with higher volatility and business risk.

Is Gold Right for You?

As with any investment, it’s important to think through your reasoning for wanting to invest in an alternative asset like gold. And if you’re curious about it, discuss it with your financial planner to see why gold may or may not align with your unique goals and time horizon.

Sources

- World Gold Council. Global Gold Demand Hits New High; Prices Soar, 2024. https://www.gold.org/news-and-events/press-releases/global-gold-demand-hits-new-high-prices-soar-2024

- European Central Bank. Focus on Central Bank Gold Holdings, 2025. https://www.ecb.europa.eu/press/other-publications/ire/focus/html/ecb.irebox202506_01~f93400a4aa.en.html

- Business Insider. Gold Price Today and Record Highs, 2025. https://www.businessinsider.com/gold-price-today-best-year-1979-bullion-record-high-2025-9

- Nasdaq. Gold vs S&P 500 Performance, 2024. https://www.nasdaq.com/articles/gold-beat-sp-500-2024-and-already-more-6-2025-should-you-buy-gold-etf-now

- State Street. Gold as a Portfolio Diversifier, White Paper, 2023. https://www.ssga.com/library-content/pdfs/insights/gold-a-portfolio-diversifier.pdf

- Buffett, Warren. CNBC Interview, 2011.

Gold just retraced from a new ATH. That high put in after a parabolic run makes it a risky buy.(in my opinion) it might need a bit of time, a few months, to consolidate and put in a double bottom before moving up again.

Good insight — gold’s price behavior often reflects both technical momentum and investor sentiment. From a diversification standpoint, we focus on its long-term role in reducing portfolio volatility over time rather than short-term moves and view gold as just one component of the broader real assets category, including real estate, precious metals and other natural resources. Appreciate you sharing your perspective.