Receiving an inheritance can feel like both a gift and a responsibility.

Whether it’s a retirement account, brokerage portfolio, life insurance, real estate, or a combination of assets, what you inherit often comes with rules, tax implications, and long-term outcomes that aren’t always obvious.

Before you make or are faced with decisions, it’s important to understand one key idea: Not all inherited assets are treated the same.

Key Takeaways

- Different inherited assets come with different tax rules, timelines, and financial considerations.

- Inherited retirement accounts, like an IRA or 401(k), are often taxable when withdrawn, while brokerage accounts and real estate may receive favorable tax treatment through a step-up in cost basis.

- Moving too quickly after receiving an inheritance can sometimes create avoidable tax consequences or missed planning opportunities.

- A thoughtful pause can help you better understand what you inherited, your options, and how these assets fit into your long-term goals.

- Inheritance decisions are often both financial and emotional, especially when family relationships or shared property are involved.

- Careful planning can help bring greater clarity and structure to decisions surrounding inherited wealth.

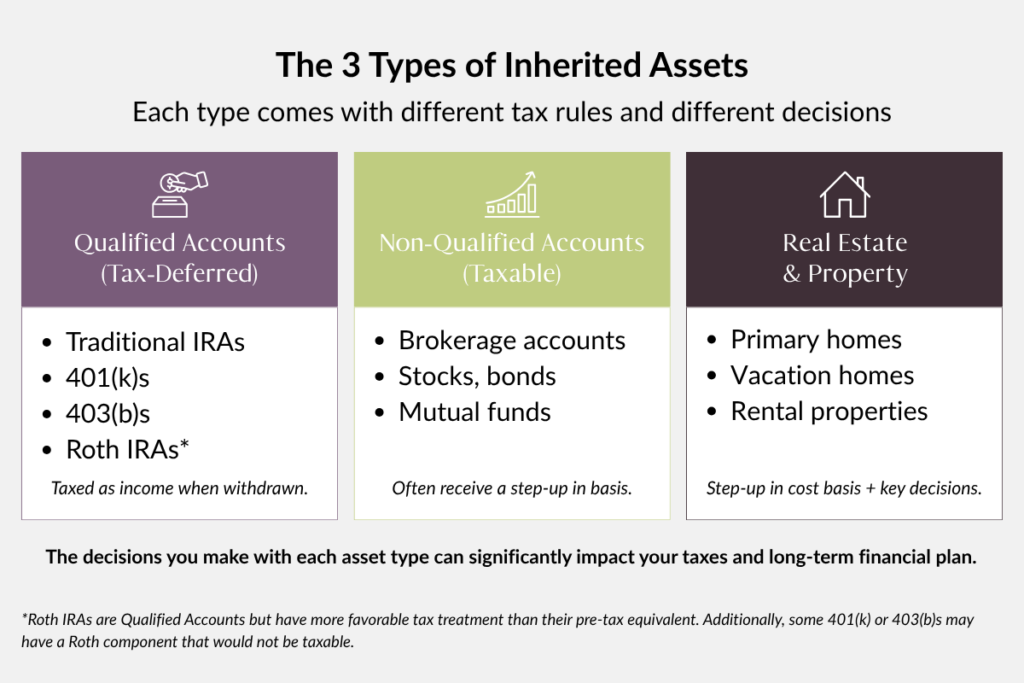

The Three Main Types of Inherited Assets

Most inheritances fall into three categories:

1. Qualified (Tax-Deferred) Accounts

These include:

- Traditional IRAs

- 401(k)s

- 403(b)s

- Roth IRAs*

These accounts have never been taxed, which means distributions are typically taxable as income.

* Roth IRAs are Qualified Accounts but have more favorable tax treatment than their pre-tax equivalent. Additionally, some 401(k) or 403(b)s may have a Roth component that would not be taxable.

2. Non-Qualified (Taxable) Investments

These include:

- Brokerage accounts

- Stocks, bonds, mutual funds

These assets often receive a step-up in cost basis, which can significantly reduce capital gain taxes.

3. Real Estate and Property

This includes:

- Primary homes

- Vacation homes

- Rental properties

- Land or undeveloped property

Like brokerage assets, these may also receive a step-up in cost basis, but often introduce additional decisions around:

- Use

- Sale

- Ongoing maintenance

- Shared ownership

- Long-term family intentions

Why the Difference Between Qualified and Non-Qualified Assets Matters

An important consideration when inheriting wealth is that different types of assets are governed by different tax rules, timelines, and planning considerations.

Two beneficiaries may inherit accounts of equal value and face entirely different financial outcomes depending on the type of asset received.

For example, inherited retirement accounts—often called qualified accounts—typically contain money that has not yet been taxed. As a result, distributions from inherited IRAs or employer retirement plans are generally treated as ordinary income. Many beneficiaries are also required to distribute these accounts within specific IRS timelines, which can be minimized with proactive tax planning.

Non-qualified assets, such as brokerage accounts or taxable investments, are treated differently. These assets often receive a step-up in cost basis at the original owner’s death, which can reduce or even eliminate capital gain tax on appreciated assets. In many cases, this creates more flexibility around timing, liquidation, and long-term investment decisions.

The distinction matters because each type of inherited asset creates different opportunities and risks.

Why the First Decision You Make Matters

One of the most common—and often most costly—mistakes inheritors make is moving too quickly.

In the days and weeks after receiving an inheritance, it’s natural to feel pressure to act. You may feel an urgency to consolidate accounts, sell investments, distribute proceeds among family members, or simply ‘take care of it’ so you can move forward. Sometimes that pressure comes from outside voices—family, friends, advisors, or financial institutions. Other times, it comes from the emotional weight of wanting resolution during a difficult season of life.

But inheritance decisions made too quickly can unintentionally create consequences that are difficult to reverse. Selling appreciated investments without understanding the tax implications, withdrawing too much from an inherited IRA in a single year, or making major financial decisions before emotions settle can lead to missed opportunities and unnecessary costs. Real estate may involve emotional attachment, family considerations, or future maintenance decisions. Even cash inheritances can raise questions around purpose, stewardship, and long-term planning.

Before making changes, it’s important to understand what you inherited, how each asset is treated from a tax and legal perspective, and how these assets fit into your broader financial life. That’s why the most important first step is often not action, but clarity. A thoughtful pause creates space to move from reactive decisions to intentional ones.

Consider Using a Decision Framework

Rather than making isolated decisions account by account, it can be helpful to step back and build a broader framework for how this inheritance will support your life and goals over time.

Understand timing. Some inherited assets come with required distribution schedules or future tax obligations that can significantly impact your financial picture. For example, taking large distributions during peak earning years may create a very different outcome than spreading them strategically over time.

Look at your current financial situation. An inheritance doesn’t exist in a vacuum. It interacts with your income, retirement timeline, investment strategy, charitable goals, and future plans. What makes sense for one beneficiary may not make sense for another, even within the same family.

Consider the role you want this inheritance to play. For some, inherited assets create security or flexibility. For others, they may become part of a retirement strategy, a way to support children or grandchildren, a philanthropic opportunity, or a legacy to preserve thoughtfully over generations.

The goal isn’t simply to ‘handle’ an inheritance well. It’s to make decisions that align thoughtfully with both your financial future and the values attached to what you’ve received.

An Inheritance Isn’t Solely a Financial Event

An inheritance is rarely just about money.

More often, it arrives during a season of grief, transition, reflection, or change. Even when assets are substantial, the experience can feel emotionally complicated. There may be gratitude alongside sadness, responsibility alongside uncertainty, or tension between honoring someone’s legacy and determining what comes next for your own life.

For many people, inherited wealth also introduces decisions they’ve never had to make before. Questions around taxes, investments, property, family expectations, or long-term planning can feel overwhelming—especially when paired with the emotional weight of loss.

Family dynamics may add another layer. Siblings sometimes approach decisions differently. One person may feel emotionally attached to a family property while another sees it primarily as a financial asset. Conversations about fairness, timing, or stewardship can quickly become personal.

Effective inheritance planning recognizes both sides of the experience: the technical realities and the human realities. And often, the best decisions come not from urgency, but from giving yourself permission to slow down, ask questions, and move forward intentionally.

You don’t have to navigate this alone.

Thoughtful planning with a financial professional can help you:

- Identify opportunities to manage tax implications

- Make informed financial decisions

- Align your inheritance with your long-term goals

If you would like to explore how Johnson Bixby may be able to assist with planning for an inheritance—or help you prepare your family through thoughtful planning strategies—please reach out.

Join Us June 23 for a Ripple Event

Receiving an inheritance can bring more than financial decisions, it can also come with unexpected emotions.

Join us for a Ripple Event, Navigating an Inheritance with Confidence, designed to help those receiving or leaving an inheritance better understand the practical and personal side of inherited wealth.

Learn more and register to attend our free Ripple Event.

Tuesday, June 23, from 5:30 – 6:30 p.m.

Frequently Asked Questions

Do beneficiaries have to pay taxes on inheritance? It depends on the asset. Retirement accounts are typically taxed as income. Brokerage accounts and property may receive a step-up in cost basis.

Is inheritance considered income? Not usually. However, distributions from inherited retirement accounts are typically taxed as income.

What should I do first after inheriting money? Pause. Understand the type of asset, tax implications, and your options before making decisions. A financial planner can help you navigate the tax considerations, timing decisions, and broader planning opportunities with greater clarity and confidence.

How long do I have to decide what to do? Timelines vary by asset type, especially for inherited retirement accounts, which may have required distribution rules.

0 Comments