The U.S. economy is poised for continued growth in 2025, building on the stronger-than-expected performance in 2024. We have a cautiously optimistic outlook on U.S. stocks due to a strong labor market and continued wage gains for consumers, the expectation of accelerating corporate earnings growth, and inflation continuing to slow. However, there are risks that need to be considered in the coming year, including equity markets trading at expensive valuations and ongoing uncertainty around changing fiscal and tariff policies.

Q4 Equity and Fixed Income Review

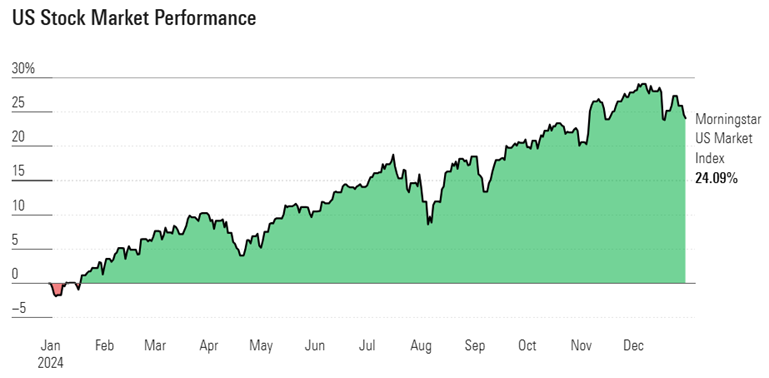

U.S. Stocks concluded 2024 on a positive note, characterized by a series of record highs in U.S. markets, driven by strong economic growth, expanding corporate earnings, and interest rate cuts by the Federal Reserve. The U.S. Market Index rebounded from a downturn in October, spending much of the quarter in positive territory as technology stocks surged. Despite a late-December decline, the index finished the quarter up 2.57% and gained 24.09% for the year.

International stocks fell in Q4, weighed down by the threat of new tariffs, a persistently strong dollar and concerns that interest rates in the U.S. may not come down as much as previously expected. Developed International and Emerging Market stocks were down over 7% last quarter, but finished the year in positive territory, up 4.93% and 7.41% respectively.

Fixed income returns experienced continued uncharacteristic volatility, with yields consistently rising throughout October. Bonds faced headwinds as progress on reducing inflation slowed, and the U.S. Presidential election results raised the potential for persistent price pressures. The U.S. Core Bond Index declined by 3.04% in Q4 but finished the year up 1.36% for the year.

Source: Morningstar Direct Data as of Dec. 31, 2024. Performance in %.

While 2024 ultimately finished with positive portfolio returns for stock investors, volatility was experienced throughout the year. The chart below shows there were numerous periods of equity market declines, with two 6% pullbacks in April and September, and a larger market correction in the second half of July. It may be helpful to remind investors that this type of volatility is very typical.

Source: Morningstar Direct. Data as of Dec. 31, 2024.

In an average year, equity investors should expect a pullback of around 5% two or three times per year and a correction of over 10% once per year, according to LPL Research. And while we are entering 2025 with the U.S. economy in a strong position and a bull market that is still young by historical standards, there is a potential for as much if not more volatility as markets adjust to the policies of a new Presidential administration, above average stock valuations and fewer interest rate cuts by the Federal Reserve.

2025, Obstacles and Opportunities

The U.S. economy entered 2025 in a position of strength, with real GDP projected to grow between 2.0% to 2.5% following a stronger than expected increase of 2.7% in 2024, according to the St. Louis Fed. The labor market is near full employment and both consumer and business confidence improved after quick resolution to the Presidential election. So, what are the risks going forward?

Obstacles: Policy Uncertainty

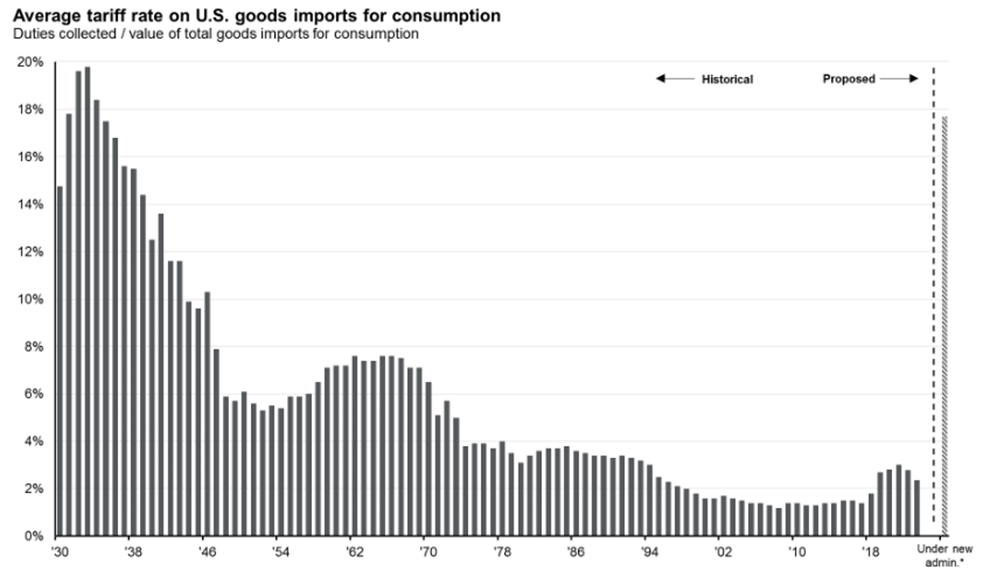

Despite the fundamentally sound economic backdrop and a significant post-election market bounce, equity and fixed income markets are exhibiting signs of concern due to policy uncertainty. While potential tax reductions and deregulation could encourage investment, tariffs might negatively impact trade and contribute to inflation. President-elect Trump has threatened 60% tariffs on all Chinese imports and 10% on imports from all other countries. If all of these were implemented tariffs would increase to the highest level in over 100 years.

Source: JP Morgan Guide to the Markets, Dec. 31, 2024.

Using history as a guide, however, tariff concerns may be a bit overblown. During President Trump’s first term, threats of “across-the-board” tariffs ultimately led to a trade deal with China and a renegotiation of the North American Free Trade Agreement (NAFTA) with Canada and Mexico. Extreme tariff threats may again simply be a negotiating tool and be much less disruptive to economic growth than currently anticipated.

Immigration is another policy uncertainty. While unemployment remains low, the labor market has come into a better balance with the overall economy making it easier for companies to find willing workers. Assuming immigration falls and deportations accelerate going forward, the recent stabilization of wage growth could reverse, leading to renewed inflationary pressures and potentially higher interest rates. There is potential for a solution from Congress that balances the needs of our economy with sensible immigration reform, which could support labor market stability, sustain economic growth, and mitigate inflationary pressures in the long term.

Opportunities: Earnings Growth

While there is a balance of risks and opportunities on the policy front, analysts are expecting corporate earnings to be even stronger in 2025 after an impressive 2024. According to FactSet, the estimated earnings growth rate for the S&P 500 is expected to be 14.9%, which is well above the 10-year average of 8%. If this rate of earnings growth does materialize in 2025, further stock market gains would be supported by fundamentals and allow large cap stocks to grow into their extended valuations.

Earnings are Expected to Accelerate

Source: FactSet, data as of 12/3/24.

Additionally, while earnings growth is expected to remain strong for the Magnificent 7 stocks of Amazon, Alphabet, Tesla, Nvidia, Microsoft, Apple and Meta, analysts are also expecting earnings growth of 21.5% and 13.9% for small and mid-cap stocks respectively. Portfolios that are well diversified and have exposure to both the largest technology stocks as well as less expensive small and mid-cap stocks could benefit from this positive earnings scenario in 2025.

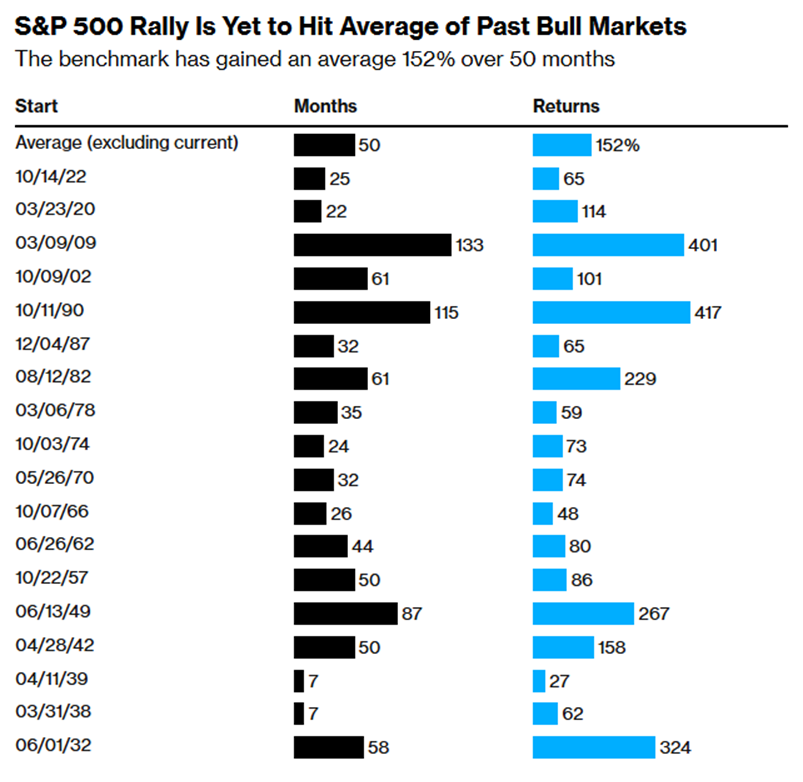

Opportunity: Baby Bull Market

While the S&P has returned over 20% for two consecutive years, the current bull market that began in October 2022 is still performing well below the average bull market experienced over the past 100 years. According to Evercore ISI, past bull markets from 1920 forward have averaged a gain of 152% over 50 months. This compares to the current bull market of around 25 months and 65% returns:

Source: Evercore ISI.

The above chart shows the current bull market could still be relatively young when comparing both duration and returns of the historical average.

Navigating 2025: Patience Amid Uncertainty and Opportunity

As in all years, investing in 2025 will bring both risks and opportunities. Investors should expect a period of elevated uncertainty which will require patience as markets adjust to changes in regulatory, immigration and tax policies from a new Presidential administration and Congress. We also see opportunities for investors which are supported by strong economic fundamentals in the U.S., a healthy labor market, accelerating earnings growth and the potential for business-friendly tax and regulatory policies supporting the continuation of this relatively young bull market.

At Johnson Bixby, we plan to navigate this backdrop of elevated uncertainty by staying disciplined and maintaining balanced, diversified investment portfolios that can weather short-term volatility and benefit from long-term opportunities. In the coming weeks, we will be paying close attention to tax and tariff policy announcements, and we are preparing to adjust client portfolios in response.

Have questions?

If you have questions about your long-term investing goals or financial planning, reach out to your financial planner for further discussion.

0 Comments