The third quarter of 2025 delivered positive returns across most major asset classes, supported by strong corporate earnings, ongoing investment in artificial intelligence (AI), and growing expectations for near-term interest rate cuts by the Federal Reserve (the Fed).

Q3 Overview

The quarter began with the S&P 500 reaching new record highs and continued with a broad rally in global equity markets, accompanied by low volatility through the end of September. Investor optimism was initially fueled by strong corporate earnings and consensus that corporations were successfully adjusting to heightened trade tensions. Toward the end of the quarter, the Fed shifted its monetary policy by cutting interest rates for the first time in nearly a year, a move seen as supportive for both equity and bond markets, pushing stock indices to further record highs.

Equity and Fixed Income Performance

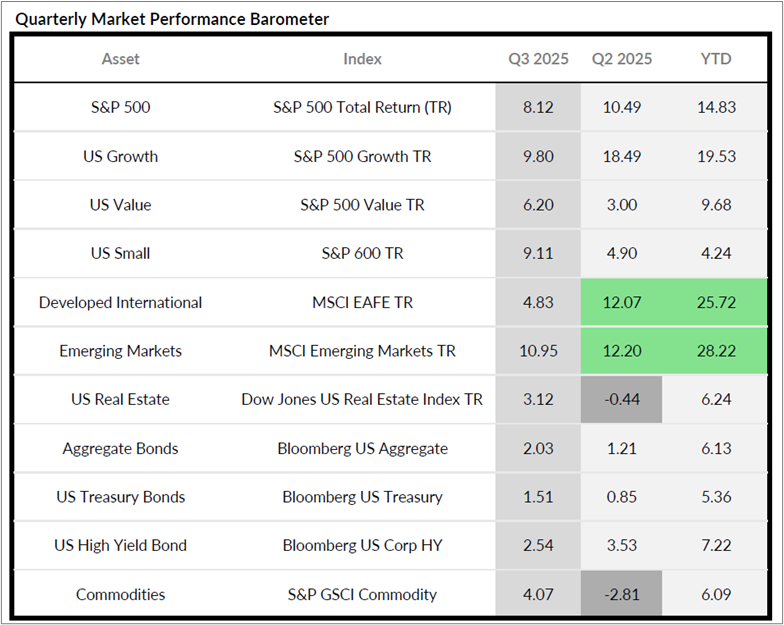

Growth stocks posted strong performance, rising 9.80% in Q3 and 19.53% year-to-date (YTD). Emerging market equities again led the market, climbing 10.95% in Q3 and 28.22% YTD, outpacing U.S. growth stocks and outperforming the S&P 500 for the third consecutive quarter. And, while developed international equities underperformed both emerging markets and the S&P 500 in Q3, they delivered a YTD return of over 25%, with the majority of gains occurring in the first half of the year.

Bond markets also delivered solid results. The Bloomberg U.S. Aggregate Bond Index gained 2.03% in Q3, buoyed by the Fed’s rate cut, which created a favorable environment for fixed income assets. Year-to-date, investment-grade corporate bonds are up over 6%, while high-yield bonds have risen more than 7%, benefiting diversified and more conservatively positioned portfolios.

Source Ycharts, Data as of September 30, 2025

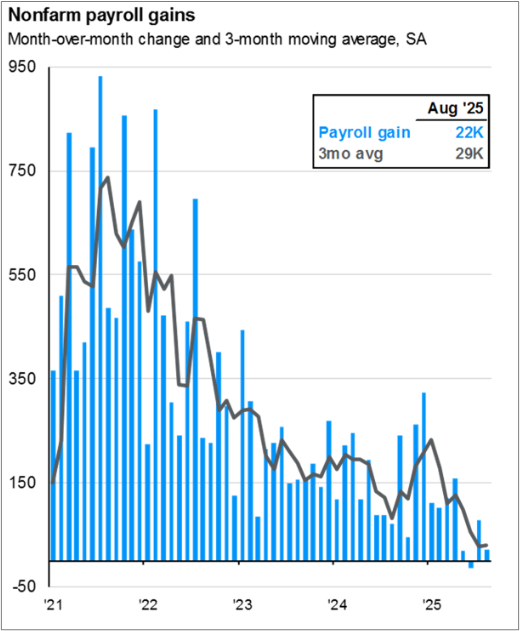

Labor Market Challenges

While most financial assets performed well in the third quarter, signs of economic weakness emerged as the quarter progressed, particularly in the labor market. Early Q3 employment reports appeared strong, reinforcing the narrative of a resilient economy despite elevated tariffs, restrictive interest rates, and persistent inflation. However, subsequent government revisions to payroll data revealed that job growth was significantly weaker than initially reported. Average monthly job gains dropped to just 29,000, and June marked the first monthly decline in employment since 2020.

Source: JP Morgan Q4 2025 Guide to the Markets

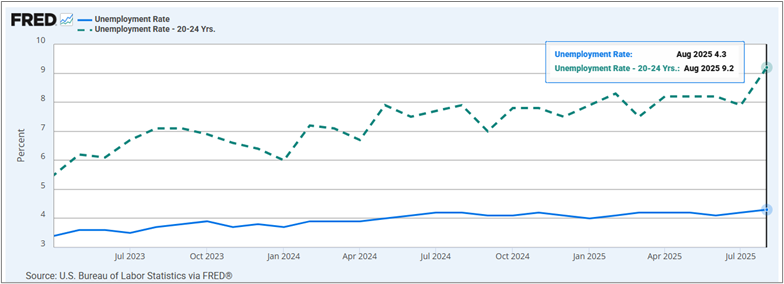

Although the overall unemployment rate remains relatively low by historical standards at 4.3%, the rapid adoption of artificial intelligence is creating headwinds for recent graduates. AI tools are increasingly automating tasks such as data entry, customer service, and other entry-level roles. As a result, the unemployment rate among individuals aged 20–24 has nearly doubled, from 5.5% in April 2023 to 9.2% in August.

Source: https://fred.stlouisfed.org/series/UNRATE

Q4 Outlook – Slowing Growth with Policy Support

As we enter the final quarter of 2025, the U.S. economy is showing signs of weakness, primarily due to sluggish job creation and a decline in consumer confidence. Despite these challenges, there are reasons to anticipate continued positive markets.

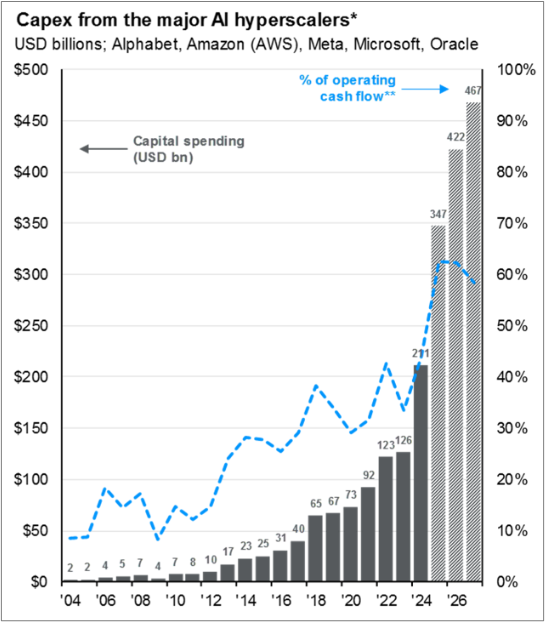

Artificial intelligence continues to be a powerful driver of economic transformation. AI-related technology spending has consistently exceeded already high expectations and is projected to grow further in the years ahead. The chart below highlights how the four largest AI infrastructure companies plan to significantly increase capital expenditures through 2027.

Source: JP Morgan Q4 2025 Guide to the Markets

While the rapid adoption of AI may be contributing to the recent slowdown in job growth, the Federal Reserve has shifted its focus toward supporting the labor market. At present, concerns about employment weakness are taking precedence over inflationary pressures. In response, the Fed cut interest rates by 0.25% on September 17. Additional rate cuts are anticipated in October and December, which could help stabilize the job market and support investment returns as we close out the year.

Looking forward, there are several crosscurrents affecting the economy and global financial markets. Inflation and tariffs, while capturing fewer headlines than they have in the recent past, continue to be potential risks for the market. Local and global politics seem omnipresent as we weather a government shutdown at home and military conflicts abroad. Meanwhile, the labor market, which had been a pillar of economic resilience, is showing signs of strain.

At the same time, corporate earnings continue to deliver positive surprises, driven by new infrastructure investment and productivity gains. Additionally, retroactive tax cuts for 2025 and more accommodative Federal Reserve policy could provide economic support as labor dynamics are coming under pressure.

As we navigate this period of heightened uncertainty and economic change, we remain committed to guiding you toward your long-term financial goals.

Have Questions?

If you have questions about your long-term investment strategy or financial planning, reach out to your financial planner for further discussion.

")

0 Comments