Rapid Recovery Amid Uncertainty

After a turbulent spring marked by sharp market declines, equity markets staged a rebound in the second quarter. In our Q2 review and Q3 outlook, we explore what drove the swift recovery, the surprising strength in international equities, and what policy shifts, earnings expectations, and global dynamics might mean for the remainder of 2025.

2nd Quarter Review

Equity markets finished a tumultuous first half of the year at record high levels after plunging almost 20% from late February to mid-April. Much of this turbulence was due to economic concerns around President Trump’s original tariff plan. Given many of the announced tariffs were ultimately delayed, a steady market rebound resulted in positive returns year to date across almost all asset classes.

Equity and Fixed Income Review

For financial markets, the second quarter started on April 2 with the announcement of new tariffs on imports. While equities were beginning to price in the expected negative impact on the U.S. economy, few were prepared for the level of duties initially proposed. The “Liberation Day” announcement intensified weakness in equity markets leading to a 10% drop in the S&P 500 over the following four days and a 19% decline from market highs in late February. However, due to market volatility, increased tariff rates were delayed on April 9, leading to a persistent and full market recovery by the end of June.

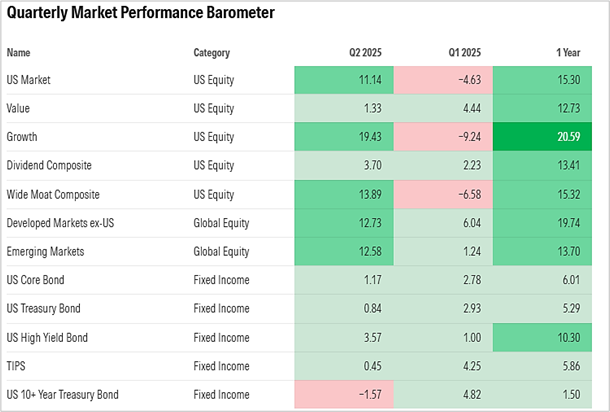

While both U.S. and international stocks saw double digit gains in Q2 2025, U.S. stocks began the quarter with negative year to date returns, but are now up over 6% through June 30. Developed International stocks outpaced all other asset classes, with a total return of 18.77% through June 30. Emerging Market equities have also outpaced U.S. stocks, finishing up over 1% in Q1 and up an additional 12.58% in Q2.

Bonds continued to perform well in Q2 2025, helping to reduce volatility for diversified investors, while providing positive inflation adjusted returns. Through June 30, U.S. Core Bonds are up just under 4%, while High Yield Bonds are up over 4.57%. Treasury Bonds, which acted as a safe haven in Q1, sold off modestly in Q2 as investors’ risk appetites increased throughout the quarter.

Source: Morningstar Direct Data as of June 30, 2025, Performance in %.

Can International Outperformance Continue?

U.S. equities have lagged international markets so far this year, after an extended period of outperformance. The chart below shows that while the S&P 500 is up over 6% in the first half of the year, international stocks as measured by the All-Country World Index, excluding U.S. stocks, are up over 18% over the same period.

Source: YCharts

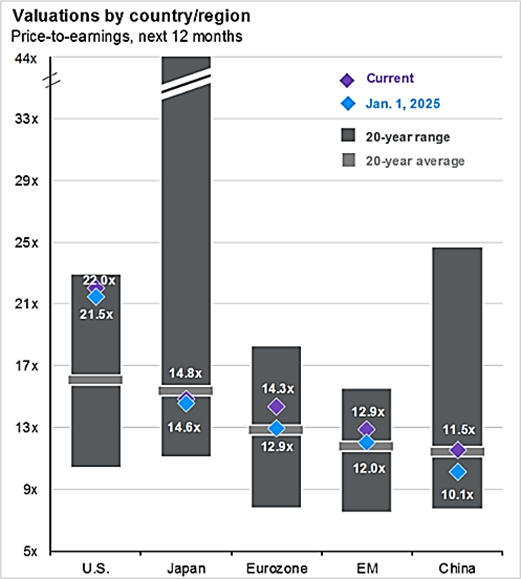

So why are international stocks outperforming and can this outperformance continue? There are several factors contributing to international outperformance, one of which is inexpensive valuations. International equities are trading at historically cheap valuations relative to U.S. equities. According to JP Morgan, while U.S. equities have an average price to earnings (PE) ratio of 22x, European equities are trading at 14.3x earnings and Emerging Market equities are trading at 12.9x earnings.

Source: JP Morgan Q3 2025 Guide to the Markets, pg. 49.

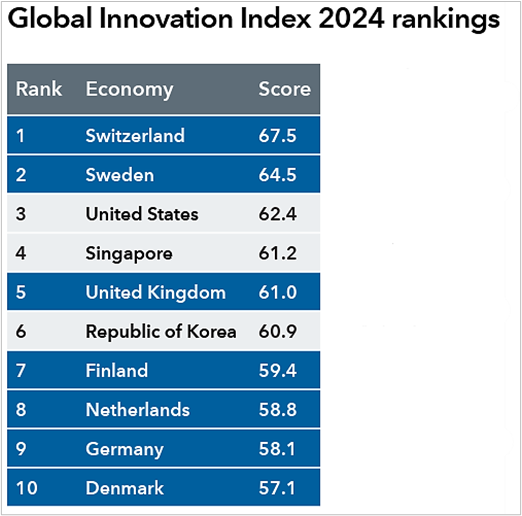

And while international equites have been inexpensive relative to U.S. equities for an extended period, some recent dynamic shifts have caused investors to increase international equity exposure. In Europe, recent agreements to increase spending on defense are expected to boost levels of GDP growth through 20281. Additionally, both Japan and Europe have been taking steps to reduce regulations in efforts to boost economic competitiveness. And while the U.S. remains a clear leader in technological innovation, seven of the top 10 countries in the Global Innovation Index are in Europe2.

Source: Capital Group 2025 Midyear Investment Outlook, pg.12.

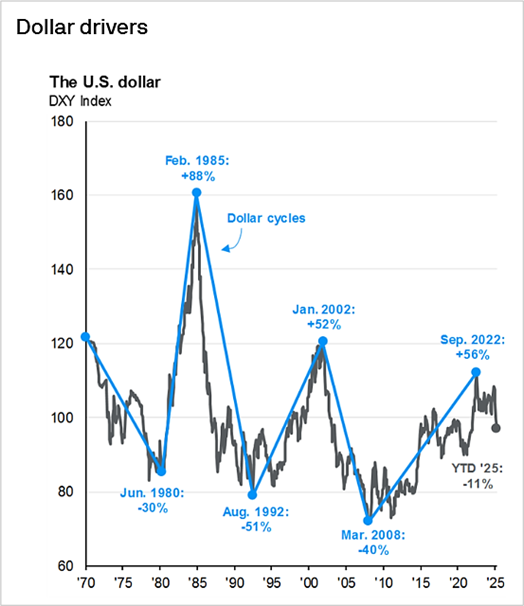

Finally, we know from history that international equities tend to outperform U.S. stocks in longer cycles that are correlated with periods of dollar weakness. And while the dollar has gone down by 11% YTD relative to foreign currencies, previous cycles have shown there is still plenty of room for continued dollar declines.

Source: JP Morgan Q3 2025 Guide to the Markets, pg. 28.

Looking Ahead: What May Be in Store for the Rest of 2025?

Despite a range of headwinds like U.S. tariffs, the Israel-Iran military conflict and other policy uncertainty, the U.S. and global economy are holding up well. While there are some signs of a slowing economy emerging, U.S. employment and household incomes remain resilient.

Additionally, while there have been interest rate cuts paired with fiscal stimulus supporting European economies, the U.S. is expected to see deregulation, more policy certainty and some stimulus from the tax legislation recently passed by both the U.S. House and Senate. Moreover, markets are expecting interest rate cuts in the U.S. by year end and into 2026 which could bolster both stock and bond markets. All of this is leading to a positive earnings outlook for the coming quarters in both the U.S. and abroad.

However, there are still plenty of reasons to remain vigilant. Tariffs, while being negotiated down, are expected to remain at their highest levels since the 1940s. And while most economists are not expecting increased tariff rates to push the U.S. or global economy into recession, the full economic effect has yet to be felt. Additionally, with U.S. equities continuing to trade at historically expensive levels, weaker than expected growth could lead to volatility reemerging and downside risk to investment portfolios.

Overall, investors should be encouraged by the resilience of the economy, financial markets and portfolio performance after this period of volatility. However, we believe it is important to maintain a sense of caution as the full effect of significant policy changes work through the economy.

Have Questions?

If you have questions about your long-term investing goals or financial planning, reach out to your financial planner for further discussion.

1 https://economy-finance.ec.europa.eu/economic-forecast-and-surveys

2 https://www.capitalgroup.com/advisor/pdf/shareholder/MFCPBR-101-1053693.pdf

Advisory services offered through Johnson Bixby, an SEC Registered Investment Advisor. Securities offered by Registered Representatives through Private Client Services. Member FINRA/SIPC. Johnson Bixby and PCS are separate and unaffiliated. The commentary expressed herein is not necessarily that of Private Client Services LLC and should not be construed as investment advice.

")

0 Comments