Updated June 2026

Whether it’s a family home, vacation property, vacant land, or a rental, inheriting property often comes with both financial and emotional considerations.

In previous articles in this series, we explored inherited retirement accounts and brokerage accounts. Property presents a different set of decisions because it can be tied to family history, memories and ongoing responsibilities.

Before deciding whether to keep, sell or transfer inherited property, consider what you’ve inherited, how ownership is structured and what responsibilities you’ve also inherited.

Key Takeaways

- The way property is titled often determines how ownership transfers after death.

- Property ownership comes with ongoing responsibilities, including taxes, insurance, maintenance and upkeep.

- Inherited property may receive a step-up in cost basis, which may reduce future capital gains taxes.

- Multiple heirs may need to work together to make decisions about inherited property.

Start with Ownership Structure

The first question to answer is: How is the property titled? Ownership structure determines how property transfers after death and who becomes responsible for future decisions.

Sole Ownership

If the property was owned by one individual, ownership typically passes according to their will, beneficiary designation (if allowed in your state), or applicable state law if no estate planning documents exist.

Joint Tenants with Rights of Survivorship (JTWROS)

With joint ownership and rights of survivorship, the surviving owner(s) become the owner(s) upon the other owner’s death.

Tenants in Common (TIC)

When property is owned as tenants in common, each owner’s share passes according to their estate plan rather than automatically transferring to the surviving owners.

This can create situations where siblings, relatives or even unrelated individuals become co-owners after a death of one owner.

Property Held in a Revocable Trust

When property is owned by a revocable living trust, the trust document governs how ownership transfers after death, often allowing assets to pass outside of probate.

Because ownership structures can significantly impact how assets transfer, it’s helpful to review property documents with an attorney or other professional advisor before taking action.

Understand Your New Responsibilities

Many inheritors focus on the value of the property but overlook the responsibilities that come with ownership.

Depending on the type of property, you may now be responsible for:

- Property taxes

- Insurance coverage

- Utility payments

- Mortgage payments, if applicable

- Maintenance and repairs

- Homeowners association dues

- Security and upkeep

Even if you plan to sell the property, these responsibilities don’t stop immediately. It’s a good idea to keep insurance in place and maintain the property to help protect its value while longer-term decisions are being made.

The Tax Advantage Many Inheritors Overlook

Like many inherited brokerage assets, inherited property often receives a step-up in cost basis. In general, the property’s basis is adjusted to its fair market value as of the owner’s date of death.

For example:

Imagine your parents purchased a home decades ago for $150,000. At the time of death, the home is worth $600,000.

If you inherit the property, your cost basis generally becomes $600,000 rather than the original purchase price. Note: this will vary based on the state you live in and how a property is registered.

This step-up in cost basis may significantly reduce capital gains taxes if the property is sold shortly after inheritance.

Because tax rules can vary based on circumstances, it’s often wise to obtain a professional appraisal and consult with qualified tax professionals before selling inherited property.

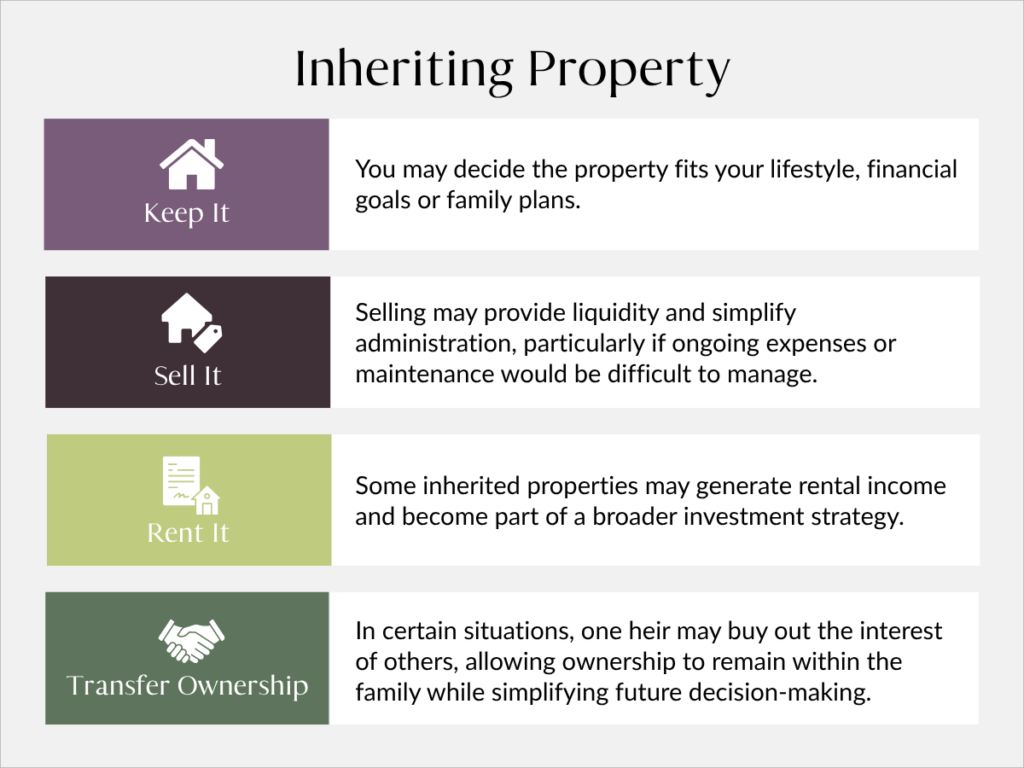

Keep, Sell, or Repurpose?

After inheriting property, many people assume they must either keep it forever or sell it immediately. In reality, there may be several viable options.

The right choice for you depends on your financial circumstances, goals and the role the property may play in your life moving forward.

What If Multiple People Inherit the Property?

One of the most common challenges occurs when multiple heirs inherit the same property. For example, three siblings may inherit a family home together.

In this situation, everyone involved may need to agree on important decisions such as:

- Whether to keep or sell the property

- How expenses will be shared

- Whether one heir wants to buy out the others

- How future maintenance costs will be handled

- Whether the property will be rented or occupied

Family members often bring different financial needs, emotional attachments and expectations to the table. That’s why clear communication can be just as important as understanding financial considerations.

Final Thoughts

Inherited property can represent both opportunity and responsibility. While tax benefits such as a step-up in cost basis may create flexibility, decisions about inherited property often involve more than finances alone. Family dynamics, ongoing costs, emotional attachment and long-term goals all play a role.

Before making major decisions, take time to understand the property’s ownership structure, value, tax implications and how it fits within your broader financial plan. A thoughtful approach can help ensure that inherited property becomes a meaningful asset rather than an unexpected burden.

You don’t have to navigate this alone.

Thoughtful planning with a financial professional can help you:

- Identify opportunities to manage tax implications

- Make informed financial decisions

- Align your inheritance with your long-term goals

If you would like to explore how Johnson Bixby may be able to assist with planning for an inheritance—or help you prepare your family through thoughtful planning strategies—please reach out.

Frequently Asked Questions

Do I pay taxes when I inherit property? Generally, inheriting property does not create an immediate income tax liability. Taxes may apply later if the property is sold and its value has increased beyond the stepped-up cost basis.

Should I get the property appraised? In many cases, yes. A professional appraisal can help establish the property’s value at the date of death, which may be important for tax purposes and future planning.

What happens if I inherit property with my siblings? You become co-owners and will typically need to work together to make decisions regarding the property’s use, maintenance and eventual sale or transfer.

Can I sell inherited property immediately? It takes time to re-register property or go through the probate process, so typically it will be 3+ months before a property can be sold. However, before selling, it’s important to understand any tax implications, ownership issues and ongoing responsibilities associated with the property. Talk to your tax advisor or financial planner.

Does inherited property receive a step-up in cost basis? In many situations, yes, though it varies by state and registration. The property’s cost basis is generally adjusted to its fair market value at the owner’s date of death, which may reduce future capital gains taxes.

Heidi Johnson Bixby is a CERTIFIED FINANCIAL PLANNER® professional and CEO and President at Johnson Bixby. Along with working directly with clients, she leads the firm’s long-term vision and mentors the financial planning team, helping ensure clients benefit from a thoughtful and coordinated planning approach. In her work with clients, she focuses on areas that continue to differentiate the firm including life transitions, retirement income design, tax planning strategies, and estate and charitable planning.

0 Comments