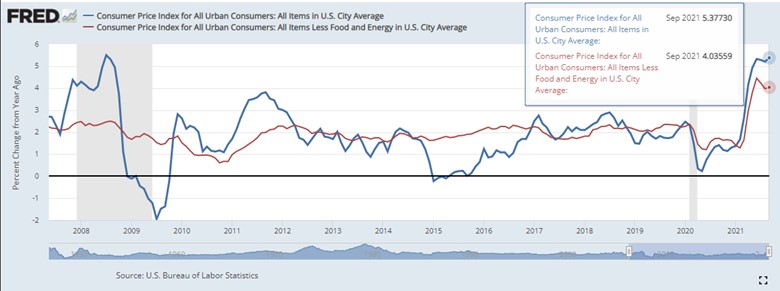

In January we published a blog titled, Now Can We Expect Some Inflation? As if on cue, inflation as measured by the Consumer Price Index (CPI) has increased steadily each month since. As shown below, the latest inflation reading measured 5.37%, well above the Federal Reserves stated target of 2%:

Concerns about inflation are understandable given daily headlines detailing rising car, gas, and food prices along with increased wage pressures. As weather turns colder, rising energy and utility costs both domestically and internationally will surely be highlighted as well. These aren’t just headlines; however, there are real world implications whether you are balancing a monthly budget, running a business, or making investment decisions.

Is Inflation Good or Bad?

If inflation is cause for concerning headlines, why is the Federal Reserve not only targeting inflation of 2%, but comfortable overshooting this mark for a period of time? Economists have argued that by cutting interest rates during a recession, the Federal Reserve can encourage economic risk-taking by corporations and higher consumer spending.

One tangible example of this effect in action is the current housing market. Low interest rates have encouraged a surge in home buying which has an economic “ripple effect.” Increased housing demand has led to new homes being built, demand for more employees to build these homes, and confident workers willing to spend more freely. However, for inflation to remain a positive economic force, corporations need be able to pass along increased business costs to maintain profit margins and wage growth needs to keep pace with prevailing price increases. In other words, excessive inflation can cut this virtuous cycle of rising employment and increased economic momentum short.

How to Invest in an Inflationary Environment

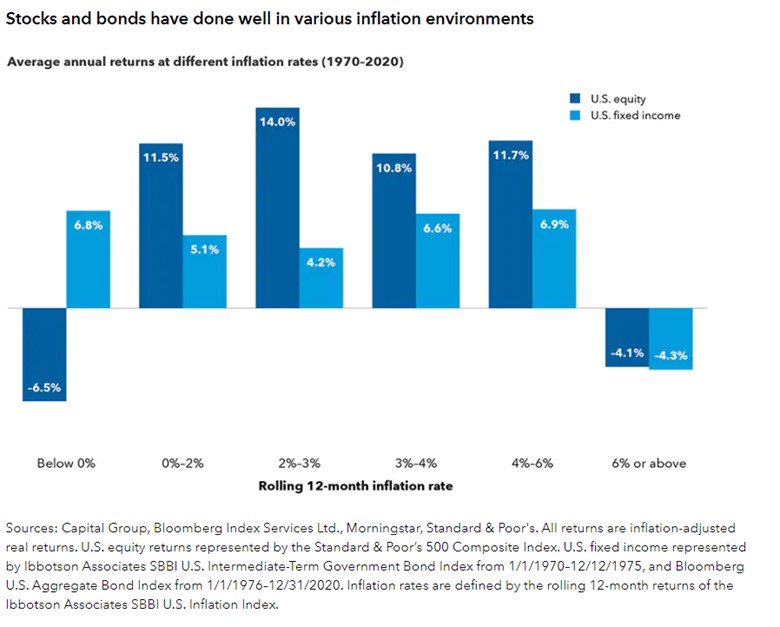

Investment portfolios can help offset rising costs due to inflation. According to a study by Capital Group, stocks and bonds historically have performed well when inflation is positive, as high as 6%:

Positioning portfolios to benefit during periods of elevated inflation can be subtle but effective. Bonds, for example, are not only paying low interest rates at present, but have had negative returns* this year as interest rates have gradually risen. Adding inflation protected, high yield, and shorter maturity bonds to a fixed income portfolio has helped offset these negative bond returns year to date.

Stock returns in general have more than kept up with inflation thus far. Having modestly higher equity exposure and adding investments in commodities enhanced those returns in 2021. If the cycle of increased employment and economic activity continues, cyclical companies tied to a growing economy in the Financial, Material, Industrial and Consumer sectors can benefit.

Looking forward, we will continue to monitor inflation and the Federal Reserve’s response and adjust portfolios accordingly to limit risks and take advantage of potential opportunities that higher rates of inflation present.

* As measured by the Bloomberg Barclays Aggregate Bond Index from January 1st-October 31st, 2021.

0 Comments