The collapse of a bank, and in this instance the failure of two U.S. lenders this past week, is of course significant. And many investors — including our own clients — are questioning what the potential impact may be for their cash deposits and investments. While these bank failures are concerning, it’s important to remember these types of events typically have little impact on your financial goals within a financial plan and an investment strategy built for the long term, with short-term volatility in mind.

What happened

The failures at Silicon Valley Bank (SVB) and Signature Bank were two of the three biggest in U.S. banking history, following the collapse of Washington Mutual in 2008. Let’s start with the facts about what has happened since last Friday, March 10:

- SVB and Signature Bank were closed and the Federal Deposit Insurance Corporation (FDIC) was appointed as receiver of both institutions.

- The FDIC guaranteed all insured and uninsured deposits at SVB and Signature Bank, and depositors have access to all their funds.

- Unlike the financial crisis of 2007-2009, equity holders are not receiving any relief, but depositors with uninsured balances are.

- Bank deposits of up to $250,000 are insured at all FDIC-insured banking institutions. Banks pay for this insurance to be able to cover deposits in cases in which they cannot for any reason.

Why it happened

Several things contributed to the demise of SVB and Signature. Let’s take a closer look at SVB, specifically.

First, the 2021-22 venture capital boom. The core of SVB’s business is the venture capital ecosystem, taking deposits from, and making loans to, VC-funded, “start-up” companies.

Second, interest rate hikes. VC funding to start-up companies was high in 2021, due to low interest rates and investors willing to invest in riskier ventures. Funding to these higher risk businesses declined in 2022 as interest rates rose.

Third, liquidity risk. Customers of SVB were withdrawing their deposits beyond what the bank could pay from its cash reserves to meet its obligations, so the bank decided to sell $21 billion of its securities portfolio at a loss of $1.8 billion. The drain on equity capital led the lender to try to raise over $2 billion in new capital.1

Fourth, the trigger point. The call to raise equity sent shockwaves to SVB’s customers and shareholders, who were losing confidence in the bank and rushed to withdraw cash.

What did SVB and Signature Bank have in common?

Both banks had huge amounts of customer deposits that were not insured by the FDIC. Of the well over $1 trillion in uninsured deposits currently in U.S. banks, Signature and SVB ranked #1 and #2.2

With so many of SVB’s customers with deposits well above the $250,000 insured by the FDIC — they knew their money might not be safe if the bank were to fail. Signature faced a similar problem, as SVB’s collapse prompted many of its customers to withdraw their deposits out of a similar concern over liquidity risk.

Are other banks next?

Questions of a run on banks have been a nagging concern. However, after the failure of the two lenders, the Federal Reserve swiftly took significant action to prevent the need for more banks to go into receivership under the FDIC should depositors quickly withdraw assets like at SVB and Signature Bank.

While banks will continue to be monitored for longer term fiscal health, a few have been popping up in the news this week.

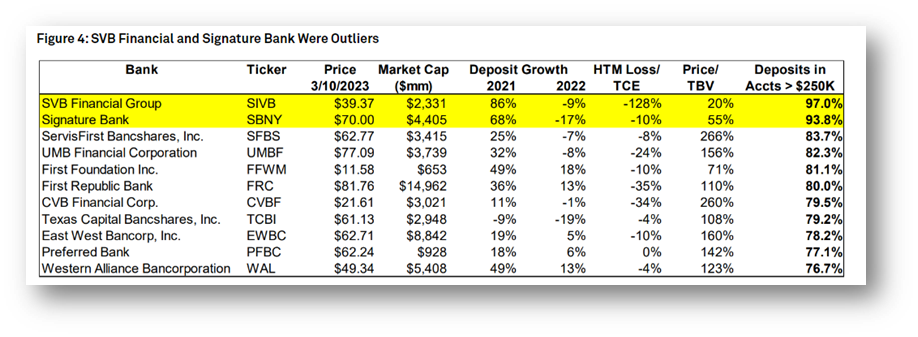

First Republic

First Republic Bank is being associated with SVB and Signature Bank for good reason. The below chart shows banks that hold a significant percentage of deposits above the $250,000 insured amount:3

That doesn’t mean the banks, like First Republic, in the above chart are next to fall. The uninsured deposit base is only a portion of the issue. Some of the other major factors SVB faced stemmed from a concentration of clientele in a high-risk, high-reward industry, as discussed above.

And, First Republic and all other banks now have the benefit of a new Bank Term Funding Program intended to help bolster bank balance sheets.

Charles Schwab

Some of our own clients who hold accounts at Schwab’s brokerage firm may be wondering about the health of the financial institution. First, investments at Schwab are held in investors’ names at Schwab’s brokerage business. Those are separate and not comingled with assets at Schwab’s Bank. The important distinction here is Johnson Bixby’s client investment portfolios are held at Schwab brokerage, not at Schwab Bank.

In regard to Schwab Bank, on Tuesday, Walt Bettinger, CEO of Schwab, said he was confident with the assets on the bank portfolio, which, again, is separate from its brokerage business.4

A few other key points came from Bettinger and Charles Schwab himself this week:5

- Schwab Bank has a broad base of high-quality customers across multiple lines of business, capital well in excess of regulatory requirements, a high-quality and relatively small loan book, and a conservative investment portfolio that is 80% comprised of securities backed by the U.S. Treasury and various government agencies.

- Collectively, more than 80% of client cash held at Schwab Bank is insured dollar-for-dollar by the FDIC. According to S&P Global Market Intelligence, that percentage is among the highest of the top 100 U.S. banks. As a comparison, the banks in the news the last few days have between 2% and 20% of their deposits insured.

- Lastly, Schwab Bank does not have any direct business relationship with Silicon Valley Bank or Signature Bank, so we do not have exposure to any direct credit risk from either.

What we’re doing

For Johnson Bixby clients, we will continue to review and monitor market conditions, and remain steady in our practice of maintaining well-positioned investment portfolios that attempt to weather challenging events and help clients meet their long-term financial goals.

Questions or concerns?

We’re here to help you have the information and perspective you need to make decisions for your long-term financial goals. If you have questions or if you’d like to review your account, please reach out to your financial planner.

1 PBS Newshour, March 14, 2023.

2 BusinessInsider, March 12, 2023.

3 FactSet, March 13, 2023.

4 Reuters, March 14, 2023.

5 Charles Schwab, March 13, 2023.

0 Comments