We’ve taken a retrospective look at first quarter market performance and other topics likely top of mind, including the latest Consumer Price Index release, and what inflation is doing, before we share a look ahead to what rising energy prices could mean, and possible actions by the Federal Reserve later this year.

1st Quarter in Review

Equity markets surged to all-time highs in the first quarter of 2024, continuing the strong momentum experienced in Q4 2023. The recession debates that economists were having last year have receded almost entirely as we see Wall Street analysts increase year-end targets for equity markets to keep pace with the current stock market rally.

Equity and Fixed Income Markets

All equity asset classes continued their upward momentum in the first quarter of 2024, with the S&P 500 breaking beyond levels last seen in November of 2021. The S&P 500 closed over 5,000 in early February and ended the quarter up over 10%. This is in addition to the 12% gain in the prior quarter. Performance was almost equally weighted between U.S. Growth and Value stocks. International and Emerging Markets returns continued to trail U.S. Equities but provided double-digit returns over the past year. After rallying dramatically in Q4 2023, bond markets have been slightly negative this year, with High Yield bonds producing the best return for the quarter.

Will Inflation Curb to Allow the Fed to Cut Rates?

Much of the above equity rally was due to resilient economic growth, a better-than-expected corporate earnings season and the expectation that interest rates will decrease at some point in 2024. The Federal Reserve, which last increased interest rates in July 2023, has indicated rates are likely at their peak and cuts will be appropriate later this year if inflation continues to moderate. The question of the moment, however, is will inflation continue coming down allowing the Federal Reserve to cut rates as expected?

While inflation as measured by CPI has come down dramatically from the June 2022 peak of 9%, progress toward the Fed’s 2% inflation target has stalled. The latest reading in March showed inflation growing at a higher-than-expected rate of 3.5%.

So, what is causing inflation to remain stubbornly above target?

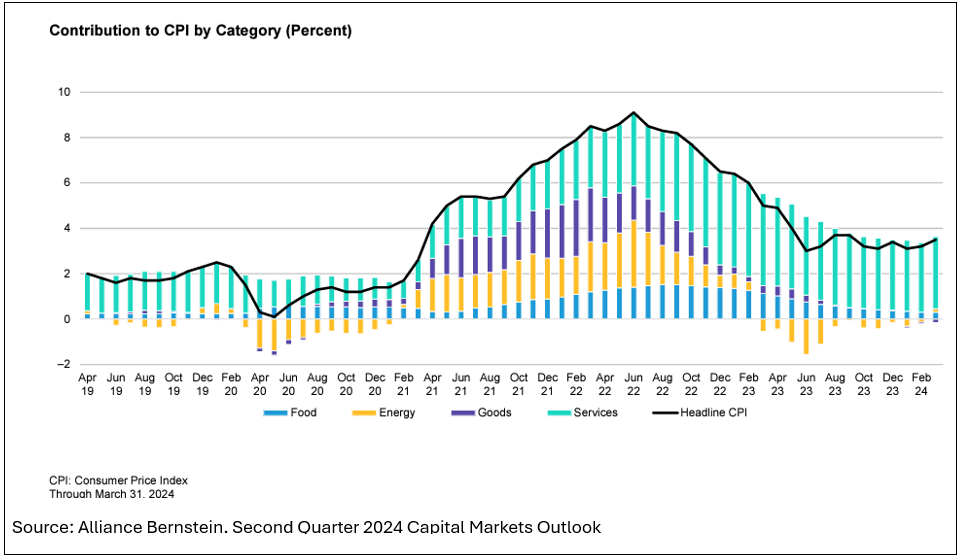

The good news is that while inflation for food, energy and goods all spiked during the pandemic, all three have fallen back to pre-pandemic levels. Services inflation, however, remains well above pre-pandemic levels. The below chart shows where inflation is currently elevated and where it has moderated.

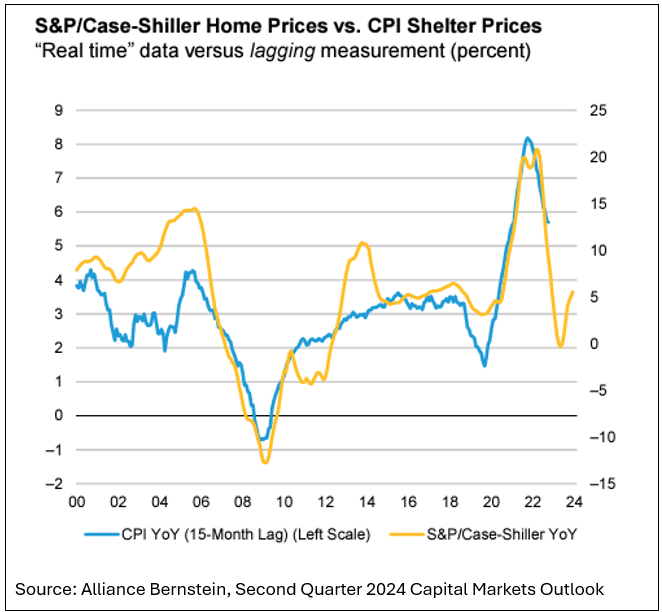

Services inflation has proven sticky. And while medical care costs and auto insurance costs have jumped over the past several months, elevated services inflation is primarily due to housing which makes up nearly 60% of this inflation component. Unfortunately, while home price inflation has fallen to pre-pandemic levels, CPI shelter price inflation remains elevated due to how it is calculated. Typically, it takes 15 months before housing price changes show up in the CPI services data.1 The below chart shows there is still reason to believe inflation can continue to fall throughout 2024, allowing for interest rate cuts later this year.

2nd Quarter Outlook

With markets trading near all-time highs and stock market valuations expensive relative to historical averages, it is fair to wonder if equities can continue their upward trend for the remainder of 2024. If inflation does resume its downward trend in the coming months and the Federal Reserve delivers on interest rate cuts this year, it is possible for markets to see continued positive performance throughout the year. Some trends bolstering this potential outcome are continued strength in the labor market, a recovery across the manufacturing sector in the U.S. economy, and an improving outlook for global growth.

Unemployment data continues to come in better than expected with the latest reading showing an unemployment rate of 3.8% and over 300,000 new jobs added in March. This may continue to support positive consumer sentiment and consumer spending. Additionally, U.S. factory activity, which has been weak since the COVID pandemic ended, unexpectedly expanded in March due to a rise in new orders. Finally, the global growth outlook has improved, partially due to the strength of the U.S. economy but also due to the understanding that most central banks are contemplating easing interest rates which can be a positive development for capital markets.

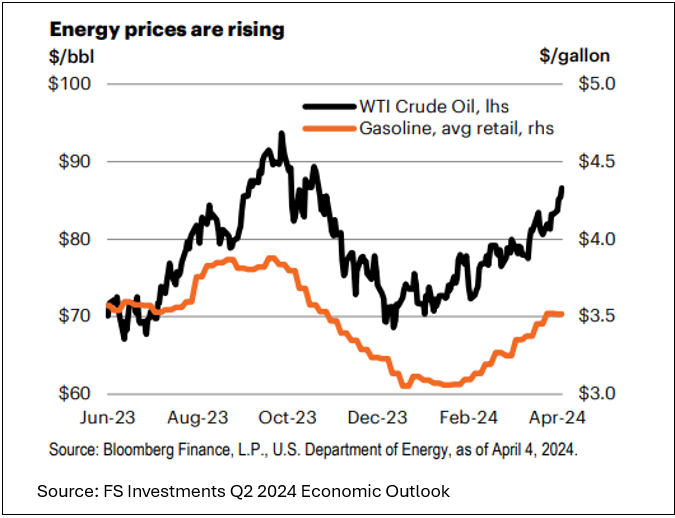

One of the largest risks to continued positive momentum, however, are rising energy prices due to geopolitical conflicts around the globe. At the beginning of April, WTI crude oil prices increased to $85/bbl (per barrel), and gasoline prices increased to $3.50/gallon. And while the current level of prices is mostly manageable for the overall economy, if prices continue up, progress on inflation could stall further and consumer confidence can deteriorate quickly.

Equity markets continue to prove strong and resilient in the current economic environment despite high interest rates. Again, this trend may continue if inflation resumes its downward trajectory, unemployment stays low and geopolitical events don’t lead to supply shocks in the energy market or elsewhere. We will continue to monitor these trends and financial markets, provide timely updates to you, and adjust portfolios as needed.

- https://www.brookings.edu/articles/how-does-the-consumer-price-index-account-for-the-cost-of-housing/

0 Comments