After Three Strong Years, What Comes Next for Markets in 2026?

Key Takeaways

- 2025 marked a third consecutive year of positive returns for diversified portfolios, with both equities and fixed income contributing.

- While valuations are elevated and the market appears later-stage, history suggests bull markets do not end simply because they are “old.”

- Looking ahead to 2026, returns may be more modest and volatility higher, reinforcing the importance of diversification and disciplined portfolio management.

2025 Was Another Positive Year for Equity and Fixed Income Markets

2025 was another strong year for diversified investors, with both equity and fixed income markets delivering positive returns. Equity markets continued to advance to multiple new market highs despite slowing economic and employment growth, supported by resilient corporate earnings, deregulation, and sustained investment in artificial intelligence (AI). Fixed income also played a constructive role in portfolios, benefiting from moderating inflation and declining interest rates later in the year.

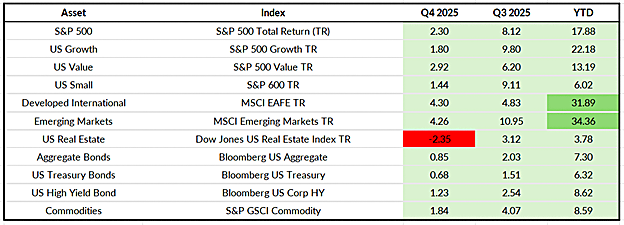

Fourth Quarter and Year to Date: Equity and Fixed Income Performance

During the fourth quarter (Q4) of 2025, equity markets extended their gains with the S&P 500 finishing the year up more than 17%. U.S. growth stocks rose 1.8% in Q4, and were up over 22% for the year, driven by continued enthusiasm around AI-related investment. Value and small-cap equities were also positive, returning 13% and 6% for the year. Despite rising tariffs on certain imports, international equities, particularly emerging markets, outperformed U.S. markets during the quarter and led on a year-to-date basis, returning over 30% for the year.

Fixed income markets also performed well in Q4 and for the entire year. The Bloomberg U.S. Aggregate Bond Index gained just over 7%, supported by falling interest rates and growing confidence that Federal Reserve policy is shifting toward supporting economic growth. High-yield and investment-grade bonds both contributed positively, highlighting the diversification benefits of fixed income within balanced portfolios.

Source: YCharts. Data as of 12/31/2025

Uncomfortably Bullish?

Bull markets often feel most uncomfortable after they have already delivered strong returns. With three years of solid performance behind us, skepticism has understandably increased. Investors are questioning whether returns like those seen since 2023 can persist and how much longer the current expansion may last.

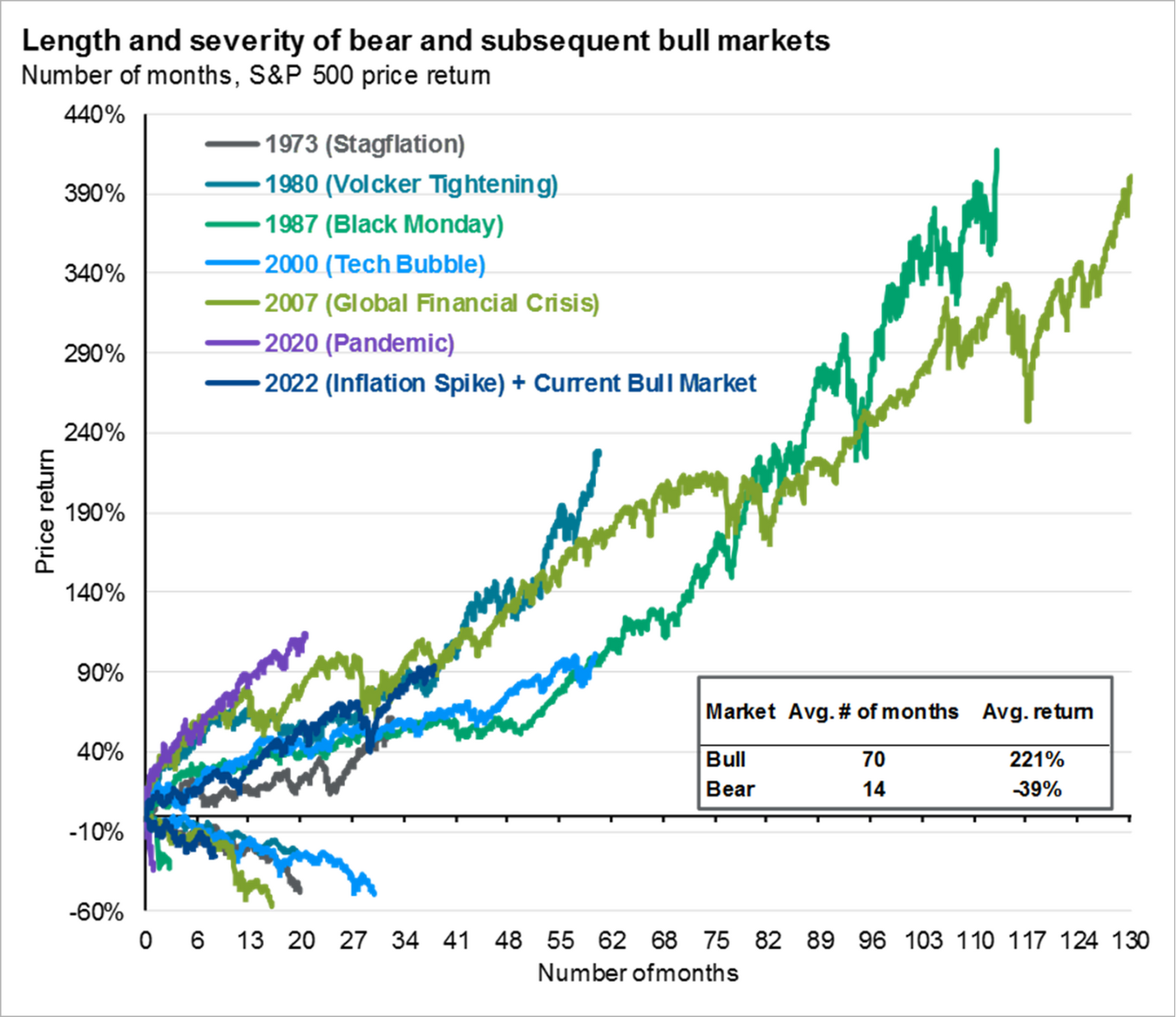

The chart below shows the duration and returns of bear markets and subsequent bull markets going back to the 1920s. Historically, bull markets have lasted an average of approximately 70 months and produced cumulative returns exceeding 200%, while bear markets have been shorter and more abrupt, lasting 14 months on average with peak losses of -39% on average. The current bull market which began on October 12, 2022, has lasted 38 months and the S&P 500 has returned nearly 100% over this period. And while past performance does not guarantee future results, this perspective helps frame where we may be in the current cycle, potentially later-stage, but not necessarily near its conclusion.

Source: JP Morgan 1Q2026 Guide to the Markets, Page 59

Beyond the fact that bull markets tend to last longer than many expect, there are additional factors that may continue to support market momentum going forward this year. First, AI-related capital expenditures continue to expand, providing a meaningful tailwind for earnings and GDP growth and may lead to a longer-term economic transformation. Also, corporate earnings, which exceeded expectations in 2025, are projected to grow by 15% in both 2026 and 2027 (Source: JP Morgan Guide to the Markets) driven partially by productivity gains from AI implementation. And while labor market growth is slowing, overall, it remains relatively stable, which can be supportive of consumer spending.

At the same time, due to the positive returns in equities over the past three years, segments of the market have become expensive relative to historical norms. While stretched valuations alone do not signal an imminent downturn, they do increase sensitivity to negative surprises and may temper future returns. As a result, disciplined portfolio construction and diversification are increasingly important.

The K-Shaped Economy

While financial markets have produced strong returns, not all investors and consumers are experiencing the same economic reality. This disconnect helps explain why investor sentiment and consumer confidence can remain muted even as equity markets reach new highs.

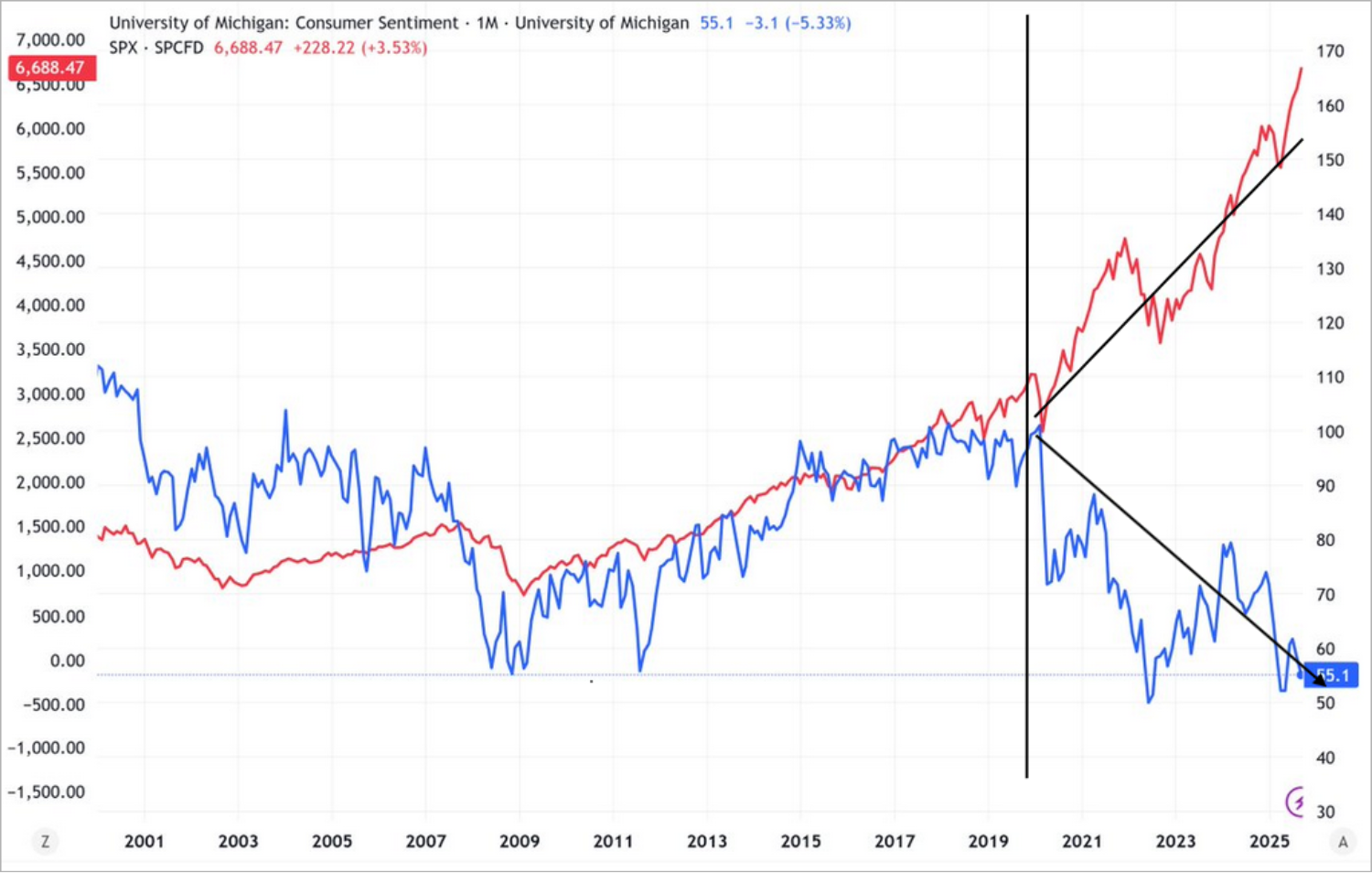

The chart below compares the University of Michigan: Consumer Sentiment Survey with the level of the S&P 500 going back to the year 2000. For much of this period, equity market levels and consumer sentiment fluctuated in similar fashion; when equity markets were up, consumer sentiment was up, with the opposite holding true as well. However, since 2020, these two measures have diverged significantly as witnessed below:

Source: https://realinvestmentadvice.com/resources/blog/the-k-shaped-economy-in-one-graph/

What is causing this change? Despite strong financial market performance over the past three years, economic outcomes have not been evenly distributed. This divergence is often described as a K-shaped economy, where some sectors, companies, and households continue to benefit from growth and rising asset prices, while others are struggling to keep pace.

On the upper arm of the K are individuals who hold larger, appropriately allocated investment portfolios, homes with low-interest rate mortgages or no mortgage, or are fully employed. They are wholly participating in the current economy due to higher wages and rising portfolio and home values exceeding the level of inflation.

The lower arm of the K consists of non-asset owners and lower income households whose wages are more exposed to consumer inflation.

This gap extends to business as well with smaller businesses struggling disproportionately under the weight of higher input costs from inflation and higher interest rates. Larger, publicly traded companies, which are less affected by higher interest rates, can invest in and benefit from technology making them more efficient and profitable over time.

And while there is no easy solution to this widening economic inequality, it does help explain how financial markets continue to produce positive investment results that contrast with many news headlines and some personal experiences.

Staying Disciplined Amid Elevated Uncertainty

Looking ahead, there are still several positive forces that can help keep markets moving forward. Company earnings remain strong, supported by productivity improvements and continued investment in areas like artificial intelligence. Inflation has cooled, interest rates have come down from recent highs, and financial conditions are more supportive than they were a year ago. And while market cycles don’t last forever, history shows that bull markets often continue longer than many expect.

That said, as we move into the next phase of the cycle, returns are likely to be more modest going forward and markets may feel bumpier in 2026. These dynamics mean staying disciplined and diversified will be even more important in the coming year.

Working closely with a financial planner to ensure your investments match your personal risk tolerance and financial needs can help keep you on track, no matter how markets behave in 2026.

")

0 Comments